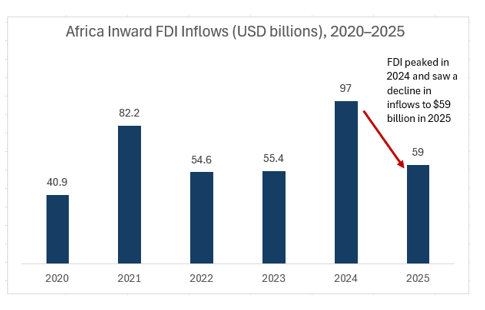

Africa recorded a historic $97 billion in FDI inflows in 2024, a 75% year-on-year increase that raised its share of global FDI from 4% to 6%, even as global FDI fell by 11% (UNCTAD World Investment Report 2025).

This marks a dramatic shift from earlier decades. In the 1970s, Africa attracted an average of just $907 million annually, rising to $1.3 billion in the 1980s and $4.3 billion in the 1990s as liberalisation opened previously closed economies (CGD, 2003). A commodity boom later pushed inflows to $98 billion in 2013, before falling back with declining oil and mineral prices (ISS African Futures). For most of this period, Africa functioned primarily as a destination for foreign capital rather than a source of it.

The question this brief sets out to answer is whether that has changed. Specifically, it examines whether capital flowing across African borders is increasingly African in origin—driven by African institutions, governments, and firms. Evidence from the past two decades suggests that it is. However, the nature, distribution, and scale of this shift require careful qualification.

Source: UNCTAD World Investment Report 2024–2025

Key Takeaway Africa’s FDI surge in 2024 reflected both genuine investor interest and heavy concentration around a small number of mega-projects. While external capital continues to dominate headline flows, the longer-term investment story increasingly lies in the growth of African-led capital deployment across sectors such as finance, manufacturing, infrastructure, and technology.

THREE ERAS: FROM EXTRACTION TO INTEGRATION

Africa’s FDI history runs in three distinct phases.The first, from the 1970s to the mid-1990s, was characterised by low investment volumes and heavy reliance on external capital. The US, UK, and France dominated inflows, largely targeting resource extraction in West and Central Africa. Although South Africa, Egypt, and Libya began investing modestly in neighbouring economies toward the end of this period, intra-African investment remained minimal.

The second phase, from roughly 2000 to 2015, saw a major shift in the sources of foreign capital. Asia’s share of Africa’s FDI stock rose from 5% in 2002 to 23% in 2018, driven largely by China, while Europe’s share declined below 50%. During the commodity boom, inflows peaked at $98 billion in 2013 before falling with global oil and mineral prices. At the same time, intra-African FDI began to rise steadily, growing from $253 million in 2001 to $23.3 billion in 2017, before reaching a record $31.8 billion in 2021.

The third phase, still unfolding today, is defined by the growing role of African corporate and institutional capital. Intra-African FDI stock increased from $19 billion in 2010 to $88 billion in 2022. By 2023, African countries accounted for 14% of investment projects across the continent, signalling a clear — though still limited — shift toward Africa investing in itself.

Key Takeaway Africa’s investment history is not a single story. It is a sequence of three eras — extraction, diversification of external sources, and the emergence of African capital — each building on the last. The third era is underway. The question is whether institutional and policy conditions can accelerate it.

A PATTERN SEEN BEFORE: ASIA AND EUROPE’S INVESTMENT TRANSITIONS

Africa is not the first region to shift from external dependence to internal capital formation. East Asia did this through the “Flying Geese” model, led by Japan from the 1960s, where rising wages and industrial upgrading pushed firms to relocate factories and production lines to lower-cost economies such as South Korea, Taiwan, and later Southeast Asia and China. These relocations transferred not just production, but also jobs, technology, supplier networks, and industrial skills, enabling recipient countries to build their own manufacturing capacity, upgrade into higher-value industries, and in turn relocate lower-value activities further down the chain over time.

Europe followed a more institution-driven version. From the 1990s, Germany and Western Europe invested heavily in Central and Eastern Europe, integrating countries like Poland, Hungary, and the Czech Republic into manufacturing value chains. EU accession and cohesion funds accelerated convergence by strengthening infrastructure, institutions, and labour capacity.

Africa is beginning to show early signs of a similar pattern. South Africa and Morocco are emerging as regional investment hubs, expanding capital and supply chain linkages into neighbouring economies. However, this progress remains constrained by weak integration architecture, including limited capital mobility, fragmented regulations, and weak cross-border enforcement.

The AfCFTA is designed to address these gaps by creating a more unified market. Whether it can do so quickly and effectively enough to shift the continent’s investment trajectory remains one of Africa’s defining policy questions.

Source: UNCTAD, 2025

Key Takeaway Japan industrialised its neighbours. Germany integrated Eastern Europe. For investors in African markets In Africa, South Africa and Morocco are beginning to play similar leadership roles as regional investment hubs and AfCFTA is the integration architecture that will determine how fast the rest follows.

THE INTRA-AFRICAN INVESTMENT GAP

African investors accounted for 14% of all investment projects on the continent in 2023, but less than 3% of total capital deployed and about 5% of jobs created (EYAfrica)This imbalance highlights a clear structural issue: African firms are increasingly investing across borders, but with limited financial capacity.

The sectoral difference is equally important. Unlike external FDI, which remains heavily concentrated in extractive industries, intra-African greenfield investments are increasingly directed toward financial services, manufacturing, logistics, telecommunications, and digital infrastructure. In simple terms, external capital extracts value, while African capital builds systems.

The scale of the financing gap is significant. The AfDB estimates Africa requires between $130 billion and $170 billion annually to address its infrastructure deficit alone. Against this benchmark, total intra-African FDI stock of $76 billion highlights the scale of the capital mobilisation still required. This mismatch shows that Africa’s key constraint is not investment activity, but insufficient capital depth. Closing this gap remains one of the continent’s most important financial challenges over the next decade.

Within this landscape, South African firms are the largest source of intra-African investment by scale, followed by Morocco and Egypt. Nigeria and Kenya are also emerging as increasingly important regional investors, particularly in banking, fintech, and telecommunications.

Source: EY Africa Attractiveness Report 2024

Key Takeaway Intra-African investment is real, growing, and structurally different from external FDI in its sectoral targeting. But it remains small relative to the continent’s needs. The opportunity for African institutions and companies to scale into that gap is the defining investment theme of the decade.

THE INSTITUTIONAL LAYER: AFDB, AFC, AND AFREXIMBANK

Africa’s key development institutions; AfDB, AFC, and Afreximbank operate at scale but remain heavily dependent on external capital. Non-African shareholders account for about 40% of AfDB voting power, while AFC and Afreximbank rely significantly on international bond markets and global institutional investors. As a result, they are African-led but not yet primarily Africa-funded, limiting their independent financing capacity.

Despite this, they are central to financing Africa’s development by mobilising capital and de-risking infrastructure and trade.

The AfDB plays a catalytic role through platforms like the Africa Investment Forum, which generated $29.2 billion in deals in 2024 and $15.3 billion in 2025. AFC directly finances infrastructure, raising over $900 million in 2025 through Samurai and Shariah facilities and co-launching a $1.5 billion infrastructure fund with AUDA-NEPAD. Afreximbank anchors trade finance, supporting systems like PAPSS, managing the $10 billion AfCFTA Adjustment Fund, and enabling growth in intra-African trade.

Together, these institutions are expanding Africa’s financial architecture by improving liquidity, reducing risk, and enabling cross-border investment and trade.

Key Takeaway AfDB, AFC, and Afreximbank are African in governance and direction. They are not yet African in capitalisation. For investors, that gap is both a risk to understand and an opportunity to fill.

THE CORPORATE VANGUARD: AFRICAN COMPANIES INVESTING ACROSS AFRICA

The strongest form of intra-African investment is corporate, not institutional. Dangote Group remains one of the clearest examples. Dangote Cement operates across multiple African markets including Ethiopia, Senegal, and South Africa, while the Dangote Refinery is expected to reshape regional fuel trade dynamics across West and Central Africa. The company’s recent $1 billion investment commitment in Zimbabwe reflects continued confidence in long-term regional demand.

South Africa’s MTN has built one of the continent’s largest telecommunications networks across 18 African countries, while Ecobank maintains operations in 36 countries, making it one of Africa’s most geographically diversified financial institutions.

Banking is the fastest-growing channel of intra-African investment, driven by high returns in underbanked markets such as the DRC. This has attracted major expansion by Standard Bank, Access Bank, UBA, and Equity Group. The implication is that intra-African investment is likely to be more durable because it is driven by commercial returns, not development policy. However, this also means investment will remain uneven, concentrated in high-return markets and sectors rather than being evenly distributed for development outcomes.

Morocco leads the most coordinated regional expansion strategy. Institutions such as Attijariwafa Bank, Banque Centrale Populaire, and Maroc Telecom are systematically expanding across West and Central Africa, reflecting a state-aligned push into regional markets. These firms are among the continent’s most active cross-border investors, signalling integration that is advancing faster than formal frameworks like AfCFTA.

Source: EY Africa Attractiveness Report 2024

Key Takeaway A growing class of African multinational firms is proving that intra-African investment can generate commercially attractive returns. These companies increasingly serve as both direct investment opportunities and broader indicators of regional economic integration.

WHAT THIS MEANS: GROWTH, JOBS, AND THE INVESTMENT MULTIPLIER

A 2025 World Bank study of 4,918 FDI projects across 24 African countries finds that investment boosts employment, upgrades skills, and generates spillovers to domestic firms (Hoekman et al., 2025). Intra-African FDI, focused on finance, manufacturing, and digital infrastructure tends to produce stronger local multipliers than extractive-sector investment, which often operates with limited domestic linkages.

Africa also has significant untapped domestic capital. Ghana and Nigeria alone hold nearly $40 billion in pension assets, over 90% of which is invested in government securities. Reallocating even a fraction into productive investments would substantially expand the continent’s internal capital base. The constraint is less capital availability than capital allocation.

THE AFCFTA VARIABLE

By January 2025, 48 African countries had ratified the AfCFTA. The World Bank estimates that full implementation could increase total FDI into Africa by up to 120% and intra-African investment by about 85%.This would lead to reduced tariffs, harmonised standards, and lower regulatory friction make cross-border investment more viable by cutting transaction costs.

PAPSS is already improving the financial infrastructure behind this integration. Historically, most African cross-border payments were routed through correspondent banks outside the continent, adding cost, delay, and currency risk. PAPSS enables direct settlement between African central banks, reducing reliance on external financial systems. Intra-African trade rose 12.4% in 2024 to $220.3 billion, recovering from a 5.9% decline in 2023. The key question is no longer functionality, but scale—how quickly adoption reaches the level where efficiency gains become self-reinforcing.

Key Takeaway AfCFTA is increasingly moving from policy ambition to operational reality. Payment infrastructure reforms, rising intra-African trade, and the gradual mobilisation of domestic institutional capital could significantly reshape the continent’s long-term investment landscape.

CONCLUSIONS

Africa’s investment in Africa is rising. From negligible intra-continental flows in the 1990s, the continent now holds $76 billion in intra-African FDI stock, a growing base of African multinationals operating across 18–36 markets, and pan-African institutions deploying capital at scale. The direction of change is clear.

The Asian and European experiences highlight what is required. East Asia aligned industrial policy with corporate expansion under the Flying Geese model, while Europe combined integration with legal certainty and cohesion funding. Africa now needs similar alignment: AfCFTA as the framework, domestic savings and pension funds as capital, and African corporates as the execution layer.

The question is no longer whether Africa can attract foreign capital—it already does. The real issue is whether African capital can be mobilised and compounded within the continent. The direction is clear; the determining factor is speed.