Africa and the global economy is experiencing another shock. This follows the growing and volatile US, Israel, and Iran conflict that started on the 28th of February 2026. This report provides the latest on Africa markets and investment landscape, covering key developments across equities, currencies, commodities, and capital flows between in the first quarter of the 2026.

This edition highlights major macroeconomic and market trends shaping Africa’s investment outlook, as well as regional performance across financial markets. It also examines commodity movements and capital allocation patterns influencing growth and investor sentiment across the continent.

A dedicated spotlight on Nigeria’s evolving tax landscape outlines the implications for both domestic and foreign investors, making it essential reading for those with exposure to Africa’s largest economy.

Special Report: The Strait of Hormuz Crisis

A distant war compounding crisis for households and businesses in Africa

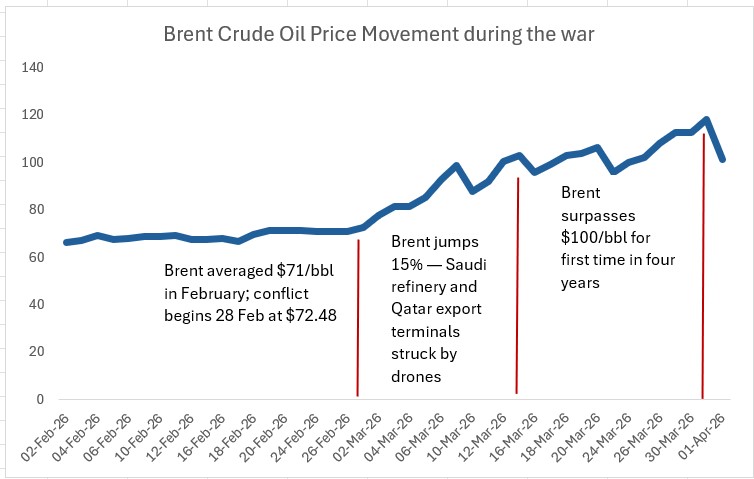

The Strait of Hormuz shock is not just a distant geopolitical event for Africa; it is an immediate economic transmission channel. From fuel prices to food costs, the effects are already filtering through the continent’s most vulnerable pressure points.

The Strait handles roughly one-fifth of global oil trade and a significant share of fertilizer exports. As tensions escalated in late Q1, oil prices rose, and supply chains tightened, triggering a chain reaction across African economies.

Fig 1: Brent crude oil price movement since 28 February 2026. Source: World Bank, 2026

What this means for Africa

For oil exporters such as Nigeria and Angola, higher crude prices support export revenues, fiscal balances, and foreign exchange inflows. But the broader continental picture is less favourable. Nearly two-thirds of Sub-Saharan Africa’s GDP comes from net fuel-importing economies, where rising oil prices feed directly into price pressures and inflation. Higher fuel costs increase transport fares, raise business operating expenses, and push up food prices in urban markets. For households, this shows up as a widening cost-of-living squeeze.

Key Takeaway: The Strait of Hormuz crisis is a dual-speed shock. Oil exporters benefit from higher prices, but most African economies, being net importers, face rising inflation, currency pressure, and growing food security risks. For households, the impact is clear: higher costs today, and potential food price increases ahead.

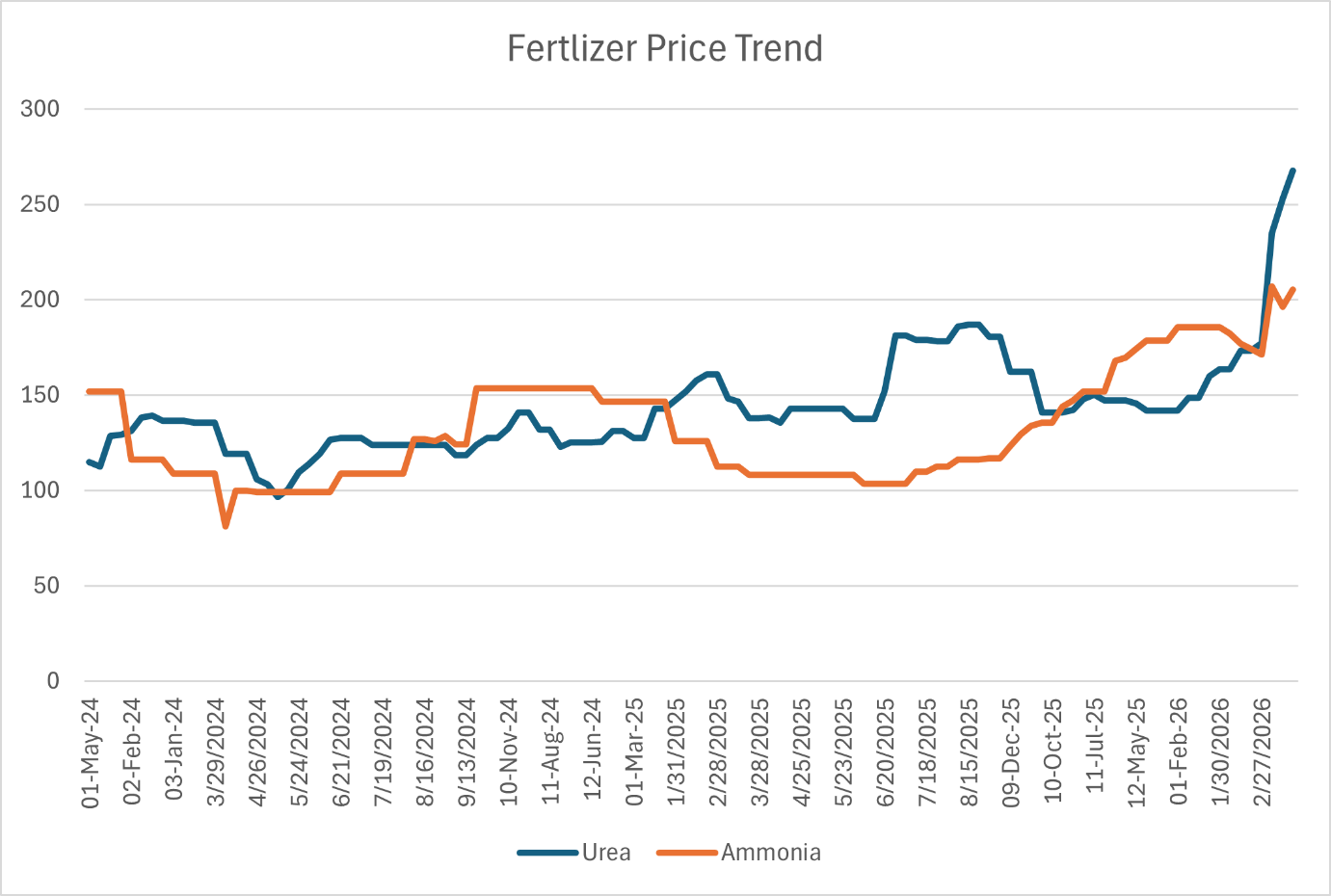

The fertilizer story: Africa’s hidden vulnerability

Fertilizer markets present an additional risk. Around 30% of globally traded fertilizer, urea, and ammonia transits the Strait, with the Gulf supplying a large share of global exports. Disruptions have pushed urea prices up by as much as 50% (IFRI, 2026) during the critical March-to-May planting season. This reflects the disruption to roughly one-third of the global fertilizer trade. Farmers are adjusting usage, increasing the likelihood of weaker harvests and higher food prices later in the year.

Fig 2: Source: Bloomberg, ABC Research 2026

Currency pressures are compounding the effect. Higher import bills are driving demand for foreign exchange, weakening local currencies and reinforcing inflation across fuel, food, and other imports.

Key Takeaway: The fertilizer crisis is arriving at the worst possible time, the March–May planting season. Farmers who miss this window face harvest shortfalls that translate into food price inflation in September–October 2026, then currency pressure, then further inflation. For investors in African consumer goods, FMCG, and agricultural stocks, this is a near-term earnings risk to model now, not when the data arrives in Q3.

The Africa Market Snapshot

Africa opens 2026 on a bull run

While global indices struggled under the weight of rising Middle East tensions and oil price spikes in late March, the S&P 500 fell roughly 1.7% in the final week of the quarter. African stock markets were experiencing all-time highs, cutting interest rates, and currencies strengthened. The continent did not move as one, but the direction was unmistakably positive.

Fifteen African central banks held monetary policy meetings in the first two months of the year. Eight of them cut rates, including Kenya, Egypt, Angola, Ghana, Mozambique, Zambia, Nigeria, and the Democratic Republic of Congo. This easing wave signals something important: after more than two years of aggressive rate hikes to fight post-pandemic inflation, African policymakers now have enough confidence to start putting growth back on the agenda.

Inflation has cooled meaningfully in several countries.In Kenya, headline inflation fell to approximately 3.5% by early 2026, well within the Central Bank of Kenya’s 2.5–7.5% target band. Ghana’s inflation declined to 12.1% in July 2025 (its lowest since December 2021) and continued moderating into 2026 despite the Bank of Ghana’s aggressive easing.. In Zimbabwe, inflation has fallen sharply from its 2024 highs following ZiG currency reforms. In Zambia, easing inflation gave the Bank of Zambia room to cut rates by 75 basis points to 13.5% in Q1 2026.

At the same time, African startup ecosystems raised $487.25 million in the first two months of 2026, an 11% increase over the same period in 2025. The composition of that money is shifting, though. Equity capital fell significantly, while debt financing more than doubled. Investors are becoming more selective and more structured. The era of easy venture money may be fading, but the demand for African solutions is not.

Key Takeaway: Africa entered 2026 with easing monetary policy, strengthening currencies across most major markets, record equity performance on its largest exchange, and a maturing startup ecosystem. The opportunity is real, but so is the need to be selective.

Equities

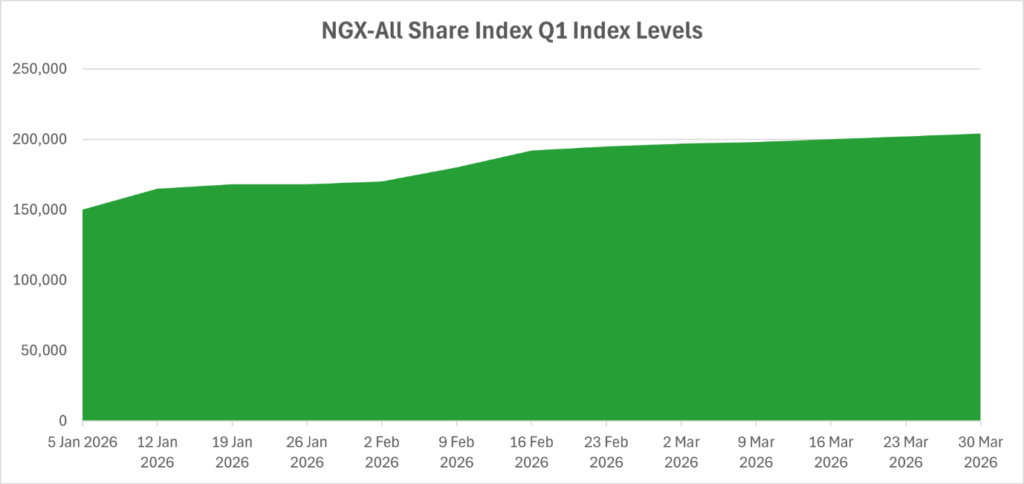

Nigeria: The NGX crosses 200,000 points, a historic first

Fig 3: The NGX All Share Index Trend

The Nigerian Exchange All-Share Index delivered the most dramatic equity story on the continent in Q1 2026. It started the year at 155,613 points and never looked back.

The rally was broad-based. Banking, consumer goods, industrials, and insurance all contributed. Foreign portfolio investors returned in force, with $3 billion in inflows recorded in January alone. What is fuelling this? A combination of falling inflation, a more stable naira, CBN monetary easing (benchmark rate cut 50bps to 27%), banking sector recapitalisation, and growing confidence in Nigeria’s macro direction.

Key Takeaway: The NGX has delivered over 29% in year-to-date returns through late March. Those who stayed in through 2024–2025 volatility are being rewarded. The question now is whether upcoming earnings can justify the new valuations. P/E moved from 14.2x in January to 16.1x in February.

South Africa: JSE hits a fresh all-time high

The FTSE/JSE All Share Index hit 126,952 points in February 2026, its highest-ever close driven by industrials, financials, telecoms, and gold miners riding bullion’s extraordinary run. The JSE’s market cap reached approximately $1.48 trillion at the peak. The SARB held its repo rate at 6.75%, noting a stronger rand and falling oil prices, which supported a benign inflation outlook.

Egypt: rate cuts and record reserves

The EGX 30 gained approximately 21.7% in Q1. The Central Bank of Egypt cut policy rates by 100 basis points in February, bringing the overnight deposit rate to 19%. Egypt’s gross reserves hit $52.74 billion at the end of February, confirmed by CBE’s official press release, reflecting its strengthened external position under the IMF programme.

Ghana: the cedi’s quiet comeback

Ghana’s cedi fell from approximately 15.60/$ at the start of the year to 10.95/$ by late March. That movement reflects both the Bank of Ghana’s aggressive easing cycle and improving macroeconomic conditions post-debt restructuring. The GSE Composite Index gained about 28.6% in Q1 2026.

Tanzania: Africa’s best local-currency equity performer

The Dar es Salaam Stock Exchange delivered a 40.65% year-to-date return in local currency making it Africa’s top-performing exchange by that measure. The Tanzanian shilling strengthened 5.71% against the dollar over the quarter. Tanzania is quietly one of the continent’s most interesting investment stories right now.

Fig 4; stock exchange return of selected market

Currencies — Q1 2026

A quarter of broad strength (with one notable exception)

The broad theme across African FX in Q1 2026 was appreciation against the US dollar. Of the sixteen major African currencies tracked in our database, most maintained or gained value in the first quarter.

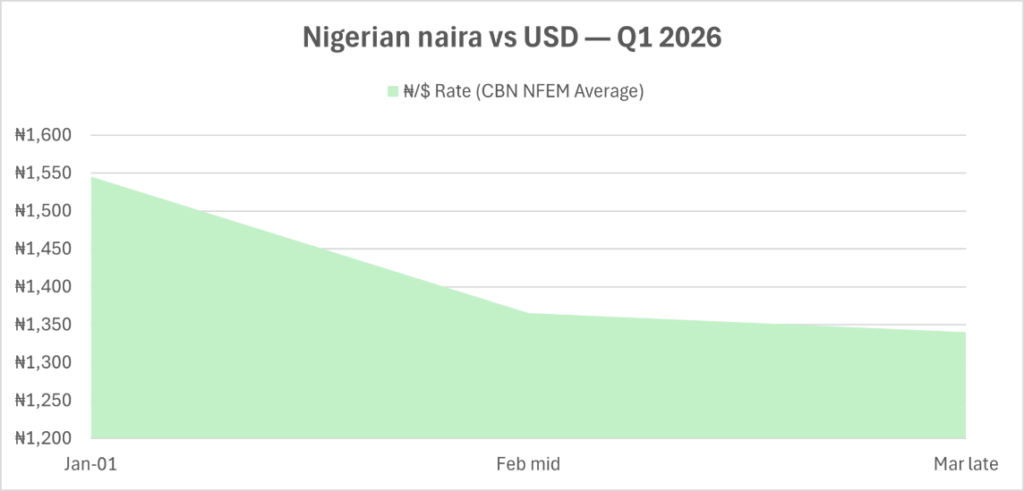

Nigeria’s naira told a nuanced story. It opened the year near ₦1,543/$ (CBN NFEM average), recovered strongly to ₦1,368.5/$ by February, and pushed below ₦1,350/$ in March, its strongest level since May 2024. Nigeria’s external reserves reached $50.45 billion as of February 16, the highest in 13 years, per CBN data, underpinning naira stability.

Key Takeaway: Most African currencies strengthened or held firm in Q1. For dollar-denominated investors, this means local-currency returns translated reasonably well into USD. For Africans with dollar-denominated liabilities, the naira’s partial recovery is good news.

Commodities & Capital Flows

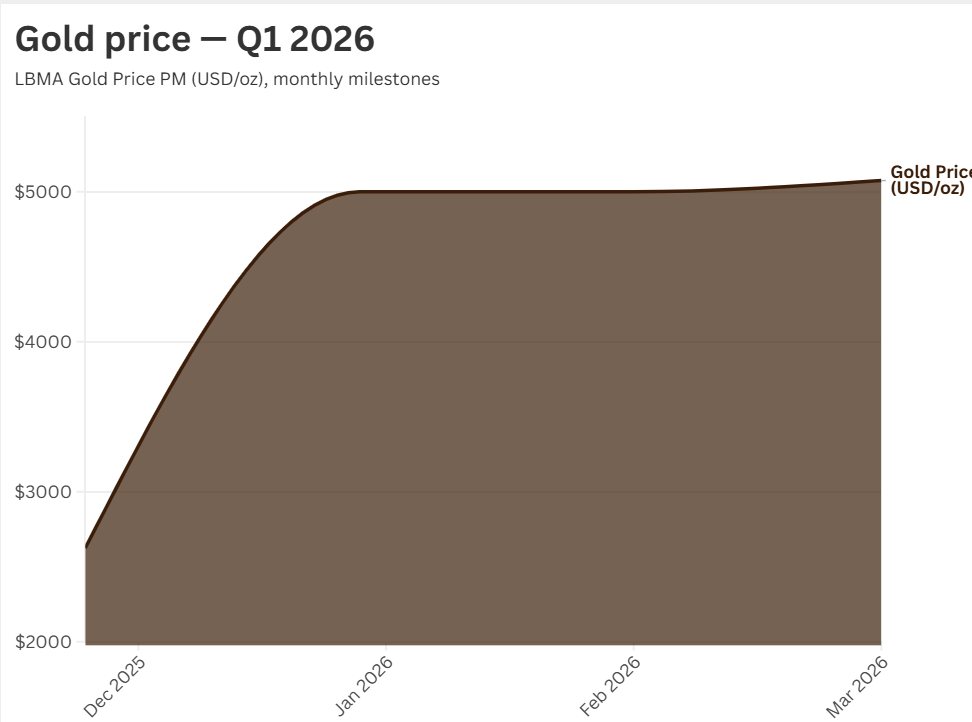

Gold: Africa’s biggest export winner in Q1 2026

Fig 5: Gold Price Trend

Gold had an extraordinary quarter globally, and African producers, particularly in South Africa, Ghana, Mali, Tanzania, and the DRC, were direct beneficiaries.

According to the World Gold Council, the LBMA Gold Price PM in USD delivered its strongest January since 1980, surging 14% in the month and closing at $4,982/oz, an all-time high. In February, the price rose another 4.8%, with gold briefly touching $5,000/oz before pulling back. By March, prices remained above the $5,000/oz threshold, supported by geopolitical tensions in the Middle East, safe-haven demand, and a weaker US dollar.

For African gold-exporting nations, this matters enormously. South Africa’s JSE rally was partially driven by gold mining stocks. Ghana’s fiscal position benefits from higher gold revenues. The WGC noted that global gold demand hit an all-time high in 2025, and central banks around the world continued buying in Q1 2026, with the People’s Bank of China adding gold for its 15th and 16th consecutive months.

Capital flows: Portfolio money in, FDI still struggling

Nigeria’s capital inflow data illustrates a continent-wide pattern. The country received $6.44 billion in foreign capital inflows in Q4 2025, a 26.6% year-on-year increase. But 85% of that was portfolio investment; treasury bills, bonds, and equities, not long-term foreign direct investment. Nigeria’s FDI for all of 2025 was just $923 million, representing less than 4% of total capital importation.

This mirrors the broader African picture. UNCTAD data shows that Africa’s FDI fell by roughly one-third in 2025 to about $59 billion, even as global FDI rose 14%. Egypt remained Africa’s top FDI destination, with approximately $11 billion in FDI. Mozambique saw an 80% surge in inflows as major LNG projects resumed. Angola returned to positive FDI territory after nine consecutive years of net divestments.

The implication is that Africa is attracting financial capital, but not yet the long-term productive capital that builds infrastructure, creates jobs, and drives durable growth. The deals that do exist are increasingly structured and DFI-backed.

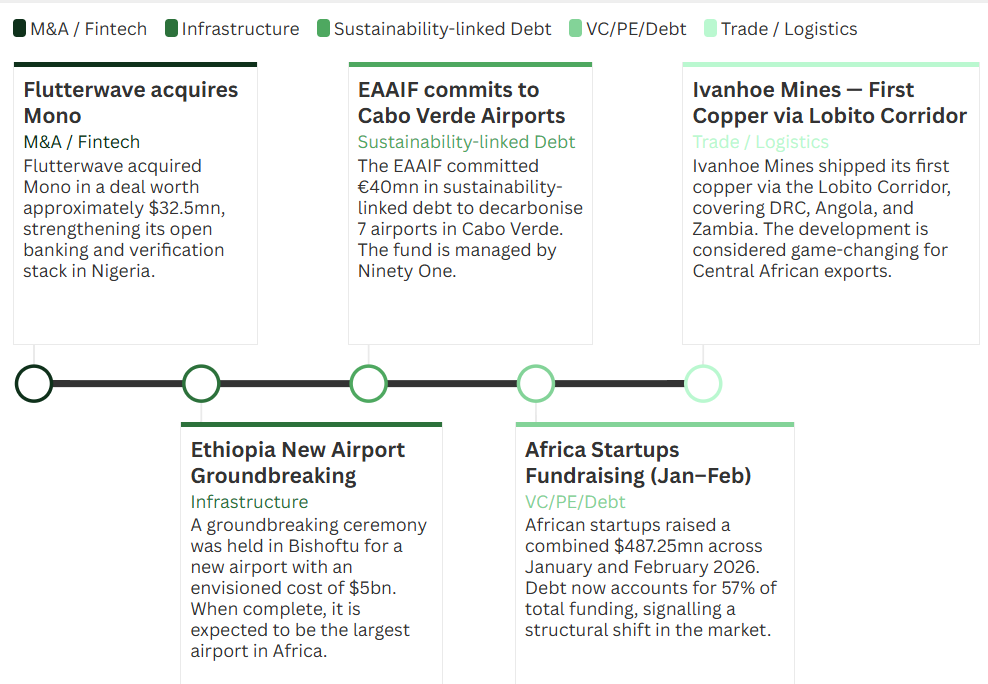

Notable deals this quarter

Several transactions defined Q1 2026’s investment landscape:

Key Takeaway: The deals getting done in Africa in 2026 are increasingly in infrastructure, healthcare, fintech, and energy, not just extractives. The Lobito Corridor shipment in particular is a landmark moment for regional integration and export capacity.

Spotlight: Investing in Nigeria

What the new tax landscape means for you

This section is particularly relevant for domestic and foreign investors with Nigerian equity, bond, or business exposure. Investors seeking to understand Nigeria’s investment tax, withholding tax, capital gains tax, or how Nigerian tax policy affects stock market returns will find this section directly useful.

Nigeria’s tax environment in 2026: What changed and what it means

Nigeria’s tax landscape shifted materially heading into 2026, and understanding those changes is now a necessary part of any investment decision involving Nigeria.

Key Takeaway: Nigeria’s tax framework for equity investors – 10% Withholding Tax (WHT) on dividends, Capital Gains Tax (CGT) exemption on listed share gains, and 0.075% stamp duty remain broadly investor-friendly at the portfolio level. The risk to watch is legislative: proposed changes to WHT or CGT can move markets quickly, as November 2025 demonstrated. For business investors, Nigeria’s 30% Company Income Tax Act and the expanding reach of the Federal Inland Revenue Service (FIRS) make professional tax advice non-negotiable.

The CBN banking recapitalization and its tax implications

Nigerian banks have completed the mandatory Central Bank of Nigeria recapitalisation exercise, with several banks raising capital through public offers and private placements – including First HoldCo’s ₦107 billion private placement, which was listed on the NGX in January 2026. For investors who participated in these offers, the tax treatment of any gains depends on the instrument and holding period. Rights issues and bonus shares are subject to specific CGT and WHT treatment under Nigerian law, and investors should confirm this with a qualified local tax adviser.

Looking Ahead:

Five things to watch

Global oil price direction. Brent crude climbed to around $112.57/barrel in the final week of March amid Middle East tensions. For Nigeria and Angola, higher oil prices improve fiscal revenue and FX inflows but may increase the cost of things, as these countries are import-dependent. For oil-importing nations like Kenya, Ghana, and Côte d’Ivoire, they create inflationary pressure and erode current account positions.

The rate cut cycle. Eight African central banks already cut rates in Q1. How far does the easing go? If global inflation re-accelerates, rising oil prices could cause some of those cuts to pause or reverse. Watch the CBN, SARB, and CBK closely.

Earnings season on the NGX. The NGX rally has pushed valuations higher. P/E ratios moved from approximately 14.2x in January to 16.1x in February. For the market to sustain momentum, Q1 earnings results need to validate those multiples. Banking, consumer goods, and telecom are the key sectors to watch.

Gold and African producers. Gold above $5,000/oz is transformative for the fiscal positions of West African and Southern African gold producers. Watch for capital allocation decisions, whether mining companies reinvest, pay dividends, or hedge.

Africa’s sovereign bond market. Sub-Saharan African sovereign bond sales reached $5.95 billion in Q1 2026, the strongest start since 2013. Zambia, Kenya, and Côte d’Ivoire have been active. The reopening of international debt markets is positive, but the borrowing cost matters. Watch spreads carefully.

Africa Invest is a monthly market commentary published by Africa Business Convention. Data sourced from the ABC Africa Investment Yearbook Database, NGX Group, JSE/FTSE Russell, the Central Bank of Nigeria, the Central Bank of Egypt, the Central Bank of Kenya, the South African Reserve Bank, the World Gold Council, ValutaFX, and African-Markets.com. This commentary is for informational purposes only and does not constitute investment advice. For full data sources and methodology, visit africabusinessconvention.com.