China has opened its market to all 53 African nations with diplomatic ties. The focus has shifted to which countries and industries will be the first to capitalize on the opportunity.

On 1 May 2026, China implemented a historic zero-tariff policy covering 100 percent of tariff lines for all 53 African nations with diplomatic ties. The policy is locked in through April 2028, marking the first time a major economy has offered duty-free access at this scale unilaterally.

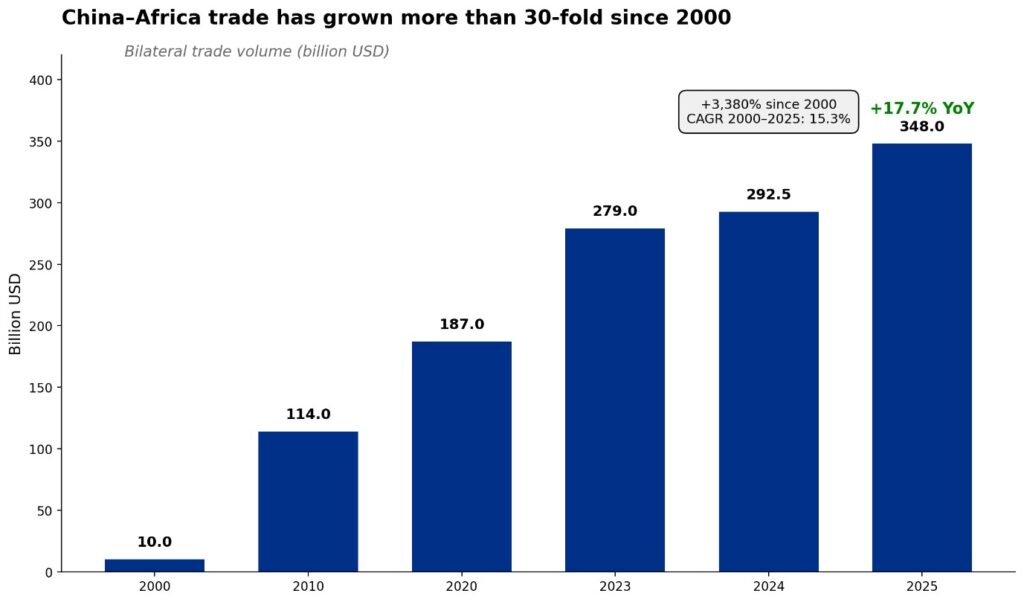

Bilateral trade reached $348 billion in 2025, up 17.7% year-on-year, with Q1 2026 data showing an additional 23.7% surge. Chinese direct investment in Africa also rose 44% in early 2026, as capital shift toward processing capacity to capture returns from the duty-free trade regime.

This reflects a structural reallocation of investment ahead of trade, as firms position to benefit from expanded market access within the limited policy window.

Fig 1: China-Africa Trade Growth, UNcomtrade data, 2025

This latest Africa investment brief analyzes the policy’s sectoral winners, structural risks, and investment implications for African markets.

I. Policy Architecture: The 2028 Horizon

This initiative expands the 2024 framework for Least Developed Countries (LDCs) to major African economies including South Africa, Nigeria, and Egypt. Crucially, the rates are guaranteed only through April 2028, aligning with the broader 15th Five-Year Plan. This creates a deliberate sense of urgency for exporters to qualify and for investors to deploy capital. To support this, China has introduced “green channels” for agriculture and new direct shipping routes to compress logistics costs.

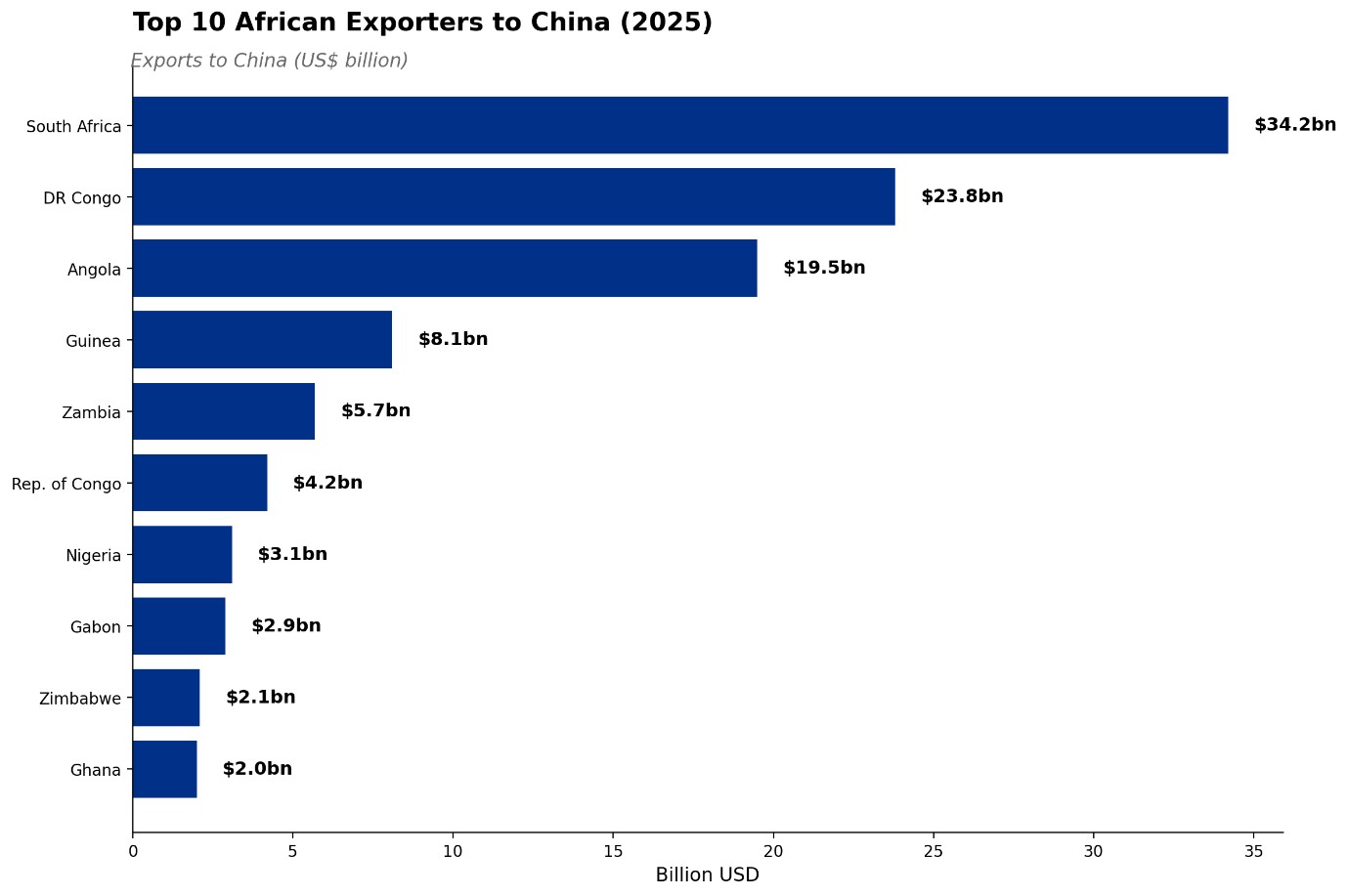

Fig 2: Top 10 African Exporters to China, UNcomtrade data, 2025

Key Takeaway: This is a time-bound trade window, not a permanent regime. Investment strategies must account for a potential reversion after 2028.

II. The Long Arc: How China’s Africa Trade Policy Has Evolved

China has been Africa’s largest trading partner for 16 consecutive years. The May 2026 announcement is the endpoint of a 25-year progression through three distinct phases.

The first phase, running from the 1990s to 2012, was driven by China’s “Go Out” policy and focused on securing oil, copper, cobalt, and bauxite while opening African markets to low-cost Chinese manufactures.

The second phase began in 2013 with the launch of the Belt and Road Initiative, which shifted the relationship from transactional commodity flows to structural integration through industrial parks, special economic zones, and supply chain financing

The third phase, from 2014 onward, marks a shift from state-led lending to market-driven integration under tighter financial discipline. After years of volatile policy-bank exposure and rising debt concerns, China has reduced reliance on large-scale concessional financing. Instead, the focus is on trade access, industrial participation, and private-sector expansion. The May 2026 zero-tariff policy is the centrepiece of this phase, replacing capital-heavy engagement with broader market integration and enabling Chinese firms to compete more directly across African value chains.

Key Takeaway: The strategy has evolved from “building the road” through massive state debt to “using the road” via private-sector trade and digital integration.

III. Chine-Africa Changing Trade Dynamics bet

Since 2000, trade between Africa and China has expanded 30-fold, but the relationship is now being reshaped by three major phases.

First, Africa’s exports are becoming more diversified. Hydrocarbons and raw minerals made up 85% of exports in 2005, but their share fell to under 70% by 2025.

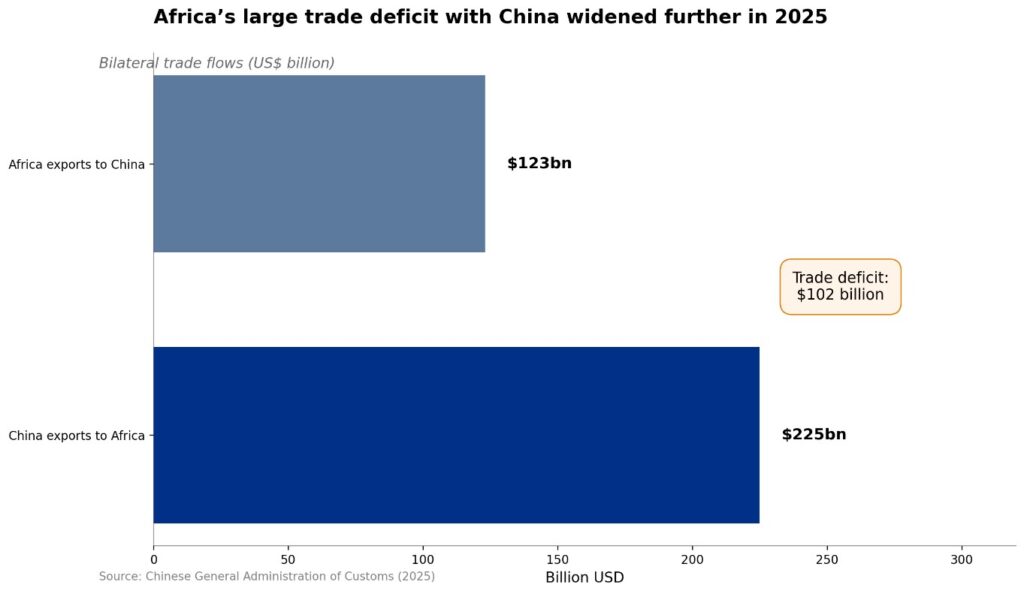

Second, Chinese exports to Africa are moving up the value chain. Electric vehicles, solar equipment, and industrial machinery helped drive Chinese exports to the continent to $225 billion in 2025.

Third, the bilateral trade deficit reached a record $102 billion last year. However, because total trade between both sides grew even faster, the deficit accounted for a smaller share of overall trade than in previous years.

Key Takeaway: The deficit is widening. The zero-tariff window is Africa’s most concentrated opportunity to narrow that gap by shifting from raw commodities to processed exports rather than just increasing volume.

IV. Regional Divergence: Africa Is Moving at Different Speeds

Africa’s economic relationship with China is not uniform. Each region is benefiting in different ways and at different speeds.

Southern Africa is the continent’s leading export bloc. South Africa exported $34.2 billion to China in 2025 about 28% of Africa’s total exports driven by a diversified mix of minerals, agriculture, and processed goods. South Africa and Zimbabwe are positioned for strong near-term gains.

Central Africa remains resource-driven. The DRC, Angola, and the Republic of Congo exported roughly $47 billion combined, largely through copper, cobalt, and crude oil. The next opportunity is local mineral processing and battery-material production.

West Africa has the biggest untapped potential. Nigeria and Ghana underperform relative to their economic size due to oil dependence and limited processing capacity. Expanding local processing could unlock major export growth.

East Africa is the fastest-growing region by percentage. Kenya, Ethiopia, Tanzania, and Rwanda are expanding exports of coffee, tea, flowers, avocado oil, and apparel, positioning the region as a rising agricultural trade corridor.

North Africa is emerging as a manufacturing platform. Morocco is building an EV supply chain, while Egypt is expanding textiles and processed goods production, supported by growing Chinese industrial investment.

Key Takeaway: Southern Africa captures margin; East Africa captures volume; West Africa requires investment to realize uplift. Investors must construct regionally-differentiated theses.

V. Sectoral Winners: Where the Margin Lives

Sectors where Chinese tariffs were previously highest capture the largest immediate gain. Agribusiness leads. Cocoa, coffee, avocado oil, citrus, wine, cashews, and dried chilli previously faced Chinese tariffs of 8 to 30 percent. At zero, they are immediately price-competitive against Southeast Asian and Latin American suppliers in one of the world’s fastest-growing premium food markets.

Beyond agriculture, Namibian lobster and Tanzanian crab now compete directly with Asian suppliers. Furthermore, the policy incentivizes in-country processing for battery minerals in Zimbabwe and the DRC, allowing these nations to export value-added materials at zero tariff. Manufacturing hubs in Egypt and Morocco are also scaling to leverage zero-cost export access for finished goods.

| Sector | Key Products | Previous Tariff → 0% |

| Agri-Processing | Cocoa (Ghana/Côte d’Ivoire), Coffee (Ethiopia/Kenya), Avocados (Kenya), Chilli (Rwanda), Ginger, Sesame (Nigeria) | 8–30% → 0% |

| Horticulture | Citrus, Wine (South Africa), Macadamia, Fresh & Dried Fruit | 10–25% → 0% |

| Marine & Aquaculture | Namibian Lobster, Tanzanian Mud Crab, Fish Products | 5–15% → 0% |

| Textiles & Light Mfg. | Processed tea, apparel (assembly hubs targeting Chinese market) | 10–20% → 0% |

| Minerals (processed) | Battery minerals — lithium and cobalt | Variable → 0% |

| Cashews & Tree Nuts | Cashew (Nigeria, Tanzania, Mozambique) | 10–15% → 0% |

Key Takeaway: Agribusiness captures the largest immediate margin gain. For investors in agro-processing and cold-chain logistics, the unit economics have materially improved. Reprice accordingly.

VI. China Trade vs. Intra-African Trade

China’s zero-tariff policy is pulling African exports outward just as AfCFTA tries to strengthen trade within the continent.

AfCFTA aims to raise intra-African trade, which still accounts for only about 15% of Africa’s total trade far below Asia and Europe. But for many exporters, China is becoming the easier market. A Kenyan coffee processor may prefer selling to China through zero tariffs, established shipping routes, and dollar settlement rather than dealing with regional logistics and currency friction within Africa.

Still, the infrastructure built for China trade such as ports, cold chains, and food safety systems could also support regional commerce. A supply chain that exports to Shanghai can also serve Lagos or Nairobi.

Key Takeaway: The policy creates short-term competitive pressure on AfCFTA ambitions. Investors should monitor investments for their regional optionality, not just their China-facing throughput.

VII. Historical Precedents: Lessons from AGOA and EBA

Africa has seen similar trade preference schemes before, most notably AGOA (the African Growth and Opportunity Act) and the European Union’s Everything But Arms (EBA) initiative.

AGOA produced concentrated winners, with a handful of countries building apparel, textile, and automotive export bases through US duty-free access. But the gains were fragile for instance when trade access was suspended or threatened, these industries contracted quickly.

EBA delivered limited results in Africa. While it boosted apparel growth in other developing regions, most African economies failed to scale due to weak processing capacity, logistics, and compliance barriers, including rules of origin and SPS standards. China’s 2010 LDC programme showed the same pattern: modest gains in agricultural exports, but no industrial transformation, as constraints were domestic rather than external.

Across all three cases, the pattern is consistent: unilateral trade access benefits economies with existing capacity, gains concentrate in a few fast movers, and reversals are costly because investment adjusts slowly.

Key Takeaway: Trade access only creates durable value where underlying industrial capacity already exists. Winners are concentrated, and those built around a single market access advantage are highly exposed when conditions change

VIII. Structural Risks for Investors

Four constraints will shape whether this policy drives real transformation or just higher trade volumes.

First, the deficit is widening. Chinese exports to Africa grew over 25% in 2025, faster than Africa’s exports into China. Without local processing capacity, zero-tariff access mainly accelerates raw material flows rather than rebalancing trade.

Second, readiness is uneven. South Africa, Morocco, Egypt, and Kenya have the industrial base and logistics to capture near-term gains. Many frontier markets remain constrained by weak ports, limited cold chains, and underdeveloped food safety systems. Tariff removal alone does not close that gap.

Third, non-tariff barriers such as rules of origin certification, product standards alignment, and regulatory requirements remain significant hurdles. Finally, currency and dependency risks are rising. Yuan settlement, reliance on Chinese capital, and persistent trade deficits offer liquidity but create dependency over time.

Fig 1: China-Africa Trade Deficit, Chinese Customs, 2025

Key Takeaway: This is a dual-speed story. Countries with existing processing infrastructure will capture immediate value-added margins, while those without supporting industrial policies risk simply expanding raw commodity exports. Investors should Favor Agro-processing leaders and avoid pure commodity extractors that lack local beneficiation strategies.

IX. The Geopolitical and Investment Outlook

China is positioning this initiative as the anchor of a South-South development architecture, contrasting with more restrictive Western trade postures. In the near term (to 2028), processed agricultural exporters in South Africa, Kenya, and Ghana see immediate EBITDA gains. Cold-chain and logistics also benefit as volumes rise, signalled by Nairobi’s first zero-tariff cargo train.

In the medium term (2028–2030, if renewed), Chinese-backed manufacturing in Nigeria, Tanzania, and Ethiopia expands exports into China, while the DRC and Zimbabwe scale battery mineral beneficiation for EV supply chains.

In the long term (post-2030), the focus shifts to Africa’s consumer market, as locally embedded Chinese firms help turn the continent from a supplier into a producer-consumer within global value chains.

Conclusion: The Door Is Open

China’s zero-tariff policy marks the most significant trade opening since the 2000 Forum on China–Africa Cooperation. Arriving as Western markets tighten, it gives Africa rare, high-volume export access at a critical moment. Current trade levels at $348 billion in volume and 23.7% growth in Q1 2026 are just the starting point of a deeper structural change

The real winners will be governments and investors that move early to build processing capacity, logistics, and compliance systems. Those who wait for confirmation will find that the most attractive entry points have already moved.