- GROWTH IS RECOVERING FASTER THAN FISCAL CAPACITY

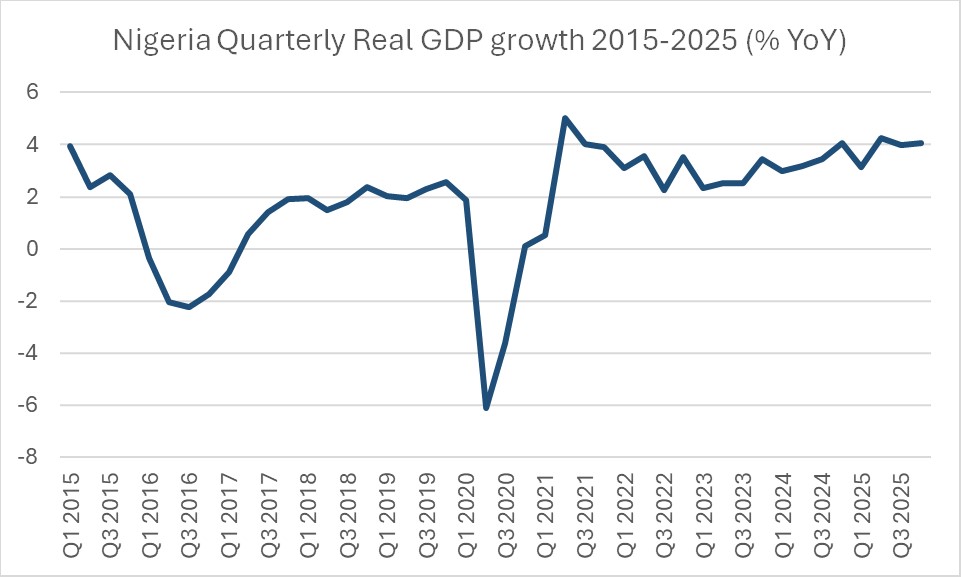

Nigeria’s economic growth trajectory has strengthened significantly since the commencement of major macroeconomic reforms in 2023. Real GDP growth accelerated from 2.31% in Q1 2023 to 2.98% in Q1 2024, 3.13% in Q1 2025, and 3.89% in Q1 2026. The IMF projects full-year growth of approximately 4.4% in 2026, positioning Nigeria among the faster-growing large economies in Africa.

Figure 1: Nigeria Quarterly Real GDP Growth (2015–2026)

Source: National Bureau of Statistics, 2026

The significance of this trend becomes clearer when viewed against Nigeria’s pre-reform performance. Between 2015 and 2022, the economy expanded at an average rate of roughly 2% annually, barely keeping pace with population growth. Investment levels remained subdued; foreign exchange shortages constrained productive activity, and significant distortions reduced the economy’s capacity to attract capital and support expansion.

The acceleration observed since 2023 did not occur in isolation.

It has been driven by a combination of reforms that addressed longstanding structural constraints, including exchange-rate liberalisation, subsidy removal, improved fiscal transparency, monetary tightening, and measures aimed at restoring confidence in the foreign exchange market. These reforms were initially accompanied by significant adjustment costs. However, they also removed distortions that had constrained investment, reduced productivity, and weakened economic competitiveness for more than a decade.

The result has been a visible improvement in macroeconomic activity. Oil production has recovered from historic lows, services activity has expanded, foreign exchange liquidity has improved, and private-sector confidence has gradually strengthened.

While no single reform can fully explain Nigeria’s growth recovery, the evidence increasingly suggests that the acceleration in economic activity is a direct consequence of the broader reform programme initiated in 2023.

The more important policy question today is no longer whether reforms have generated growth. The question is whether that growth can now be translated into stronger fiscal capacity, reduction in poverty, and creation of jobs for millions of Nigerians.

This is where the next phase of reform begins.

Despite stronger economic activity, government revenues continue to lag expenditure requirements. Consequently, fiscal conditions remain considerably tighter than macroeconomic indicators alone would suggest.

Key Takeaway

The Nigerian economy is growing at roughly twice its pre-reform trajectory. The challenge facing policymakers is no longer restoring growth momentum but ensuring that growth translates into sustainable public revenues and fiscal strength, reduction in poverty, and the creation of jobs in millions.

- THE DEBT STORY IS MORE COMPLEX THAN THE HEADLINE NUMBERS

Nigeria’s public debt stock stood at approximately ₦159 trillion at the end of 2025. Viewed solely in naira terms, this appears to represent a dramatic increase over a relatively short period. However, naira-denominated debt figures provide only a partial picture of what has occurred. A closer examination shows that a substantial portion of the increase reflects accounting recognition and currency revaluation rather than equivalent levels of new borrowing.

Figure 2: Nigeria Total Public Debt Trend (2023–2025) in Naira and Dollar Terms

Two developments are particularly important.

First, approximately ₦30 trillion in Ways and Means advances previously extended by the Central Bank of Nigeria were formally recognised and securitised. These obligations already existed within the public sector balance sheet but had not previously been fully reflected within conventional debt reporting frameworks. Their inclusion improved transparency and strengthened fiscal reporting standards, but it should not be interpreted as fresh borrowing undertaken during the period.

Second, exchange-rate reforms significantly altered the naira valuation of Nigeria’s external debt obligations.

As the naira adjusted to market realities, the domestic currency value of existing foreign-currency debt increased substantially. Although the underlying dollar obligations remained broadly unchanged, their reported naira equivalent expanded considerably.

Consequently, a large share of the increase in reported public debt reflects valuation effects rather than new debt accumulation. This distinction becomes evident when debt is viewed in both naira and US dollar terms. While naira-denominated debt appears to have expanded sharply, the increase in dollar-denominated debt has been significantly more moderate. In fact, the dollar series suggests a far less dramatic debt trajectory than commonly portrayed in public discourse.

This does not imply that debt-related concerns are misplaced.

Public debt has increased; fiscal deficits remain elevated, and refinancing pressures continue to warrant careful monitoring. However, the evidence does not support the simplistic conclusion that Nigeria accumulated the entirety of the reported increase through new borrowing over the past three years.

The more accurate interpretation is that reported debt growth reflects a combination of new borrowing, enhanced fiscal transparency, and exchange-rate revaluation. For investors and policymakers, the critical issue is therefore not the headline debt number itself, but whether economic growth and revenue mobilisation can expand rapidly enough to support debt-service obligations over time.

Key Takeaway

The popular narrative that Nigeria’s debt simply tripled within three years because of borrowing overlooks two major factors: the formal recognition of previously existing obligations and the exchange-rate revaluation of external debt. The more relevant fiscal question is not how large the debt stock appears in naira terms, but whether revenues and growth are expanding sufficiently to sustain it.

Figure 3: Sources of Increase in Public Debt Stock.

| Driver | Approximate Contribution |

| Ways & Means Recognition | ₦30 trillion |

| Exchange Rate Revaluation | Approx ₦40 trillion |

| Net New Borrowing | Residual Balance |

CLOSING NOTE

Nigeria’s fiscal debate is often framed as a choice between optimism and concern. The evidence suggests that both perspectives capture part of reality. Growth is strengthening. Investment conditions are improving. Reform momentum remains significant.

At the same time, debt service obligations are rising, fiscal space remains constrained, and revenue mobilisation has yet to fully catch up with the scale of the economy. The defining question for the next phase of Nigeria’s economic story is therefore not whether growth will occur.

It is whether that growth can be successfully converted into fiscal capacity, reduction in poverty, and the creation of jobs in millions.

The answer will determine not only the trajectory of public finances, but also the country’s ability to sustain investment, accelerate development spending, and fully realise the gains from one of the most consequential reform programmes in its recent history.