Last week, Nigeria’s foreign reserves crossed the US $40 billion-mark, first time since October 2019. Nigeria’s reserves have seen tremendous growth this year following the rapid and sequential rate rises by the Central Bank Monetary Policy Committee (MPC). Our estimates show that since the MPR started to rise in February 2024 from 18.75 percent to the current 27.25 percent, the Bank has attracted about US $8 billion in foreign portfolio flows.

The performance is even more remarkable given that the new leadership of the Central Bank under Olayemi Cardoso inherited a doubtful exchange rate level of about US $33 billion and has paid off an estimated US $7 billion in outstanding backlogs.

Fig. 1 The Monetary Policy Rates’ steep rise since February 2024

The Nigerian economy has relied on increases in MPR to attract foreign portfolio flows given that the government has not been able to ramp up oil production in the short term. Ramping up oil production from the current trajectory of 1.4 million bpd is the country’s best route to medium- and long-term economic stability, growth, and jobs. The foreign direct investment element also takes time to respond and particularly responds to economic stability as well.

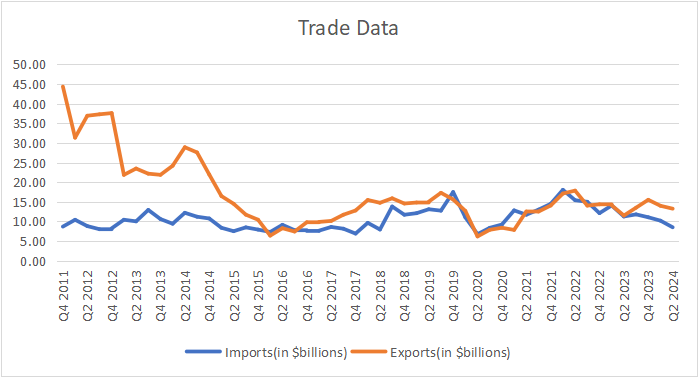

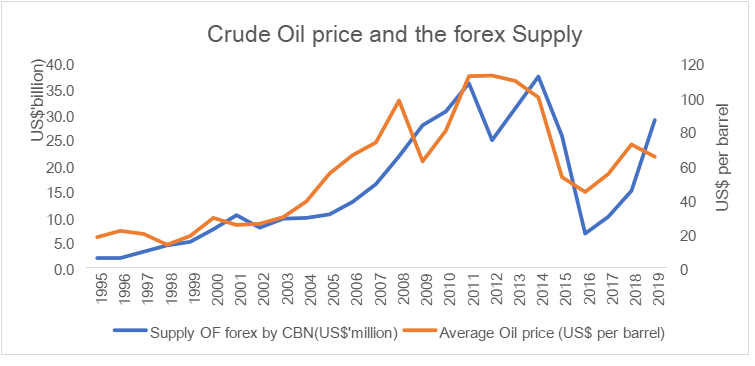

As fig. 2. shows, while our imports are relatively stable, the value of our exports have falling dramatically since 2010. In 2020, Nigeria produced 2.8 million bpd while we currently half of that today. While it is also a reflection of the price of oil, the main reason for the decline in the value of exports is the decline in the volume of oil exports. It is not surprising that the supply of foreign exchange mirrors the value of oil exports. See fig. 3.

Fig.2. Nigeria’s total exports and imports in US dollars since 2011.

The recent presentation by Olu Arowolo Verheijen, the special adviser to the President on Energy, buttresses the point that attracting FDI takes time. She said, “we have unlocked over US $1 billion in investments across oil and gas value chain, and by the middle of 2025 we expect to see final investment decisions (FID) on two new projects, including a multibillion-dollar Deepwater exploration project.”

Fig. 3 The dynamics of oil prices and the supply of US $

Challenges remain though. The central bank cannot continue to rely on the rise in interest rate and other monetary policy measures for containing inflation and attracting foreign exchange. Indeed, the reason it has not been very successful is the poor coordination and collaboration from the fiscal side. As reported in the statements by the members of the monetary policy committee, fiscal deficits and debts are currently higher than planned for the year. It means that despite increases in the revenues, the federal government has not been able to contain its expenditures to planned levels.