A year after his appointment as the governor of the Central Bank of Nigeria (CBN), Olayemi Cardoso has come the same conclusions as many of his predecessors – Nigeria’s successful monetary policy is dependent on appropriate fiscal policies, measures, and programmes.

For instance, in his presentation after the monetary policy committee in September, the governor said:

“Members (monetary policy committee) therefore reiterated the need to work in close collaboration with the fiscal authority to address the current upward pressure on energy prices. The MPC noted the continued growth in money supply, recognizing the need to curtail excess liquidity in the system as well address foreign exchange demand pressure. Members were also concerned about the growing level of fiscal deficit but acknowledge the commitment of the fiscal authority not to resort to monetary financing through ways and means. Furthermore, members observed a strong correlation between FAAC releases and liquidity levels in the banking system as well as its impact on exchange rate.”

From this statement, it is not only clear that current macroeconomic stability measures of the Bank are hindered by fiscal policy measures but that there is a lingering mindset in the government at all levels that the solution to all problems is to spend. This mindset is also responsible for the poor choices made when it comes to expenditure.

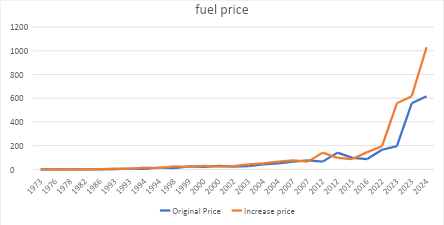

While energy prices are rising following the removal of subsidies, it been exacerbated on the back of the volatility and weakness of the exchange rate that arises from pressures from FAAC releases.

Fig. 1. Changes in fuel prices showing dramatic changes since June 2023.

As also shared above, the growth in money supply and excess liquidity in the financial system, exerting pressures on prices and exchange rate, also originates from fiscal expenditures. The governor also expressed concern over the growth in deficit financing of the budget.

After his appointment in September 2023, Yemi Cardoso has set to do three major things – fight the twin elements of macroeconomic instability in exchange rates weakness and volatility, and inflation, strengthen the country’s financial system, and clean the rot in the apex bank in relation to lose monetary policy arising from development banking.

By suspending all development banking measures, the governor has cut the over N10 trillion liquidity through credit subsidies, and strengthening the banking system through the ongoing new capital requirements. However, establishing macroeconomic stability remains a tough challenge.

Notwithstanding, the Bank, under Cardoso’s leadership, has grown the country’s external reserves by nearly 20 percent since September 2023, with reserves up from the US $33 billion in 2023 to US $39 billion in September 2024.

The macroeconomic instability challenge is also a common theme in the analysis provided by all monetary committee members in their statements released last week. It is on the basis of this that all members of the MPC voted to raise the monetary policy rate by 50 basis points from 26.5 percent to 27.25 percent except Philip Ikeazor, the deputy governor in charge of financial stability, according to the personal statements released by the Bank last week,

To see the changes in the Nigeria’s debt dynamics since the Q1 2024, ThinkBusiness Africa checked the debt data releases on the debt management office (DMO) website. It observed that the latest data for Q2 2024 has not been released. It thus means that for this first in this decade, the subsequent quarter has elapsed without the releases of the latest debt data for the previous quarter. If this persists, doubts will begin to set in about whether the government is hiding the latest data of deficits and debts or seeking to manipulate the level of deficits and debts as done under President Muhammadu Buhari when the government hid the data on ways and means until the twilight days of his administration. Since June 2019, all debt data releases were done in the middle of the following quarter.