IMF extends Egypt loan to 2026, releasing $2.3 billion to bolster reserves

By: ThinkBusiness Africa The International Monetary Fund (IMF) said on Wednesday that its Executive Board has successfully completed the combined fifth and sixth reviews of Egypt’s economic reform program. The decision unlocks approximately $2.3 billion in fresh financing for the North African nation, providing a critical buffer as it continues to navigate a complex path toward macroeconomic stability. The total package consists of two distinct funding streams designed to address both immediate fiscal needs and long-term structural resilience. Under the Extended Fund Facility (EFF), roughly $2 billion will be disbursed following the completion of the fifth and sixth reviews of Egypt’s 46-month loan program. Similarly, under the Resilience and Sustainability Facility (RSF) program approximately $273 million was approved under a separate review focused on climate-related and long-term structural reforms. This latest move brings total disbursements under Egypt’s current IMF arrangements to roughly $5.2 billion. To ensure the momentum of these reforms, the IMF also confirmed an extension of the EFF arrangement through December 15, 2026. In a statement following the board meeting, the IMF praised Cairo’s “sustained stabilization efforts,” noting several key improvements in the country’s macroeconomic profile. Annual urban consumer inflation, which peaked at 38% in late 2023, declined to 11.9% by January 2026. With Real GDP growth accelerating to 4.4% in the 2024/25 fiscal year, up from 2.4% the previous year. Foreign Reserves rose to $59.2 billion as of December 2025, supported by a shift to a flexible exchange rate and significant foreign direct investment (FDI). “Tight monetary and fiscal policies, together with exchange rate flexibility, have helped restore macroeconomic stability and strengthen the external position,” the Fund noted. Despite these gains, the IMF cautioned that progress on structural reforms has been “uneven.” Specifically, the Fund highlighted the slow pace of the government’s divestment agenda—a key pillar of the deal aimed at reducing the state’s footprint in the economy to allow for more private-sector-led growth. Egypt’s loan program was originally set at $3 billion in late 2022 but was expanded to $8 billion in March 2024. The expansion was triggered by severe external shocks, including the conflict in Gaza and disruptions in the Red Sea, which slashed Suez Canal revenues—a vital source of foreign currency—by nearly 50% in early 2024. The government has recently taken bold steps to meet IMF benchmarks, including a significant cabinet reshuffle and a EGP 40 billion social protection package aimed at shielding the most vulnerable from the impact of high prices.

Zimbabwe rejects $367 million U.S. health deal over “unequal” data sharing terms

By: ThinkBusiness Africa The government of Zimbabwe has officially terminated negotiations with the United States over a proposed $367 million bilateral health funding agreement. The collapse of the talks, announced Wednesday, centers on a dispute over “data sovereignty” and the sharing of sensitive biological information. Government spokesperson Nick Mangwana stated that the deal, which would have provided funding over five years for HIV/AIDS, tuberculosis, and malaria, was rejected because it required Zimbabwe to hand over comprehensive epidemiological data and virus samples without guaranteed access to future medical breakthroughs. According to Zimbabwean officials, the proposed Memorandum of Understanding (MoU) was “asymmetrical.” The government argued that the U.S. was seeking long-term access to Zimbabwe’s biological resources but refused to reciprocate data sharing — Washington allegedly would not share its own epidemiological data in return. Zimbabwe sought assurances that its citizens would have access to any vaccines, diagnostics, or treatments developed using the shared data—a request they say the U.S. denied. “In essence, our nation would provide the raw materials for scientific discovery without any assurance that the end products would be accessible to our people should a future health crisis emerge,” Mangwana said in a statement. The United States has been Zimbabwe’s largest health donor for two decades, providing nearly $2 billion since 2006. The U.S. Embassy in Harare expressed regret over the decision and confirmed it will now begin the “difficult task” of winding down its health assistance. Zimbabwean authorities characterized the rejection as a move toward protecting national security and a preference for multilateral frameworks. They argued that “virus data with pandemic potential” should be managed through the World Health Organization (WHO) rather than through bilateral deals with “strings attached.” While U.S. Ambassador Pamela Tremont noted that Zimbabwe has indicated it is prepared to manage its HIV response independently, the sudden loss of the country’s primary donor raises concerns about the stability of a healthcare system already under significant strain.

Zimbabwe Imposes immediate ban on all raw mineral and lithium exports

By: ThinkBusiness Africa In a major policy shift aimed at curbing “malpractices” and forcing domestic industrialization, the Zimbabwean government has suspended the export of all raw minerals and lithium concentrates with immediate effect. The Ministry of Mines and Mining Development said on Wednesday, that the suspension remains in place until further notice and applies even to minerals currently in transit. The sudden directive accelerates a long-standing government plan to shift the economy from basic extraction to high-value processing. While Zimbabwe had previously set a deadline of 2027 to ban lithium concentrate exports, today’s announcement brings that timeline forward by nearly a year. “Government remains committed to ensuring transparency, in-country value addition, and beneficiation,” said Mines Minister Polite Kambamura in a statement. “This measure has been taken in the national interest to curb leakages and enhance efficiency within our systems.” He said. Under the new regulations:Only companies with valid mining titles and approved, functional in-country beneficiation plants will be permitted to export. Agents and third-party traders are no longer authorized to export minerals on behalf of mining firms as security and revenue agencies, including the Zimbabwe Revenue Authority (ZIMRA), have been ordered to block all unprocessed consignments, including those already on their way to ports. The news sent ripples through global commodity markets, particularly for lithium—a critical component in electric vehicle (EV) batteries. Zimbabwe holds Africa’s largest lithium reserves and has become a primary supplier to China. In response to the news, shares of major Western lithium producers like Sigma Lithium, Albemarle, and Lithium Americas saw significant gains in pre-market trading, as investors braced for potential supply tightening from Southern Africa. The move follows years of criticism from civil society and economic analysts who allege that billions of dollars in mineral wealth are lost annually through smuggling and undervalued raw exports. The ban leaves several major mining operations in a precarious position. While some Chinese-backed firms, like Huayou Cobalt and Sinomine, have already begun commissioning local processing plants, many smaller and mid-sized miners still rely on exporting raw ores to stay afloat.

Dangote Refinery engages 12 major marketers to end Nigeria’s fuel Imports

By: ThinkBusiness Africa Aliko Dangote, President of the Dangote Group, has confirmed a massive offtake agreement with 12 major petroleum marketers. The deal secures the daily distribution of up to 65 million litres of Premium Motor Spirit (PMS) across the country, effectively meeting the entirety of Nigeria’s domestic demand. The agreement marks the end of decades of reliance on imported fuel and positions Nigeria as a burgeoning energy hub in Africa. The framework, endorsed by the Nigerian Midstream and Downstream Petroleum Regulatory Authority (NMDPRA), establishes a structured supply chain to eliminate the “middleman” bottlenecks that have historically plagued Nigerian fuel markets. Domestic Supply of 60–65 million litres per day exceeds Nigeria’s daily consumption estimated at 50–60 million litres; leaving 10–15 million litres to be exported to international markets. The 12 marketers include industry giants such as NNPC Retail, MRS Oil, TotalEnergies, 11 Plc (formerly Mobil), Ardova Plc, and Rainoil, among others. During the announcement in Lagos, Aliko Dangote revealed that the refinery’s operational capacity has surpassed its nameplate design. While the plant was built to handle 650,000 barrels per day (bpd), recent live data showed the facility reaching an output of 661,000 bpd. “We have agreed on an offtake framework to supply up to 65 million litres daily for the domestic market. This is a decisive break from the era of fuel scarcity and foreign exchange volatility,” Dangote stated. Analysts suggest this move will have a profound effect on the Nigerian economy. By ending petrol imports, Nigeria will save billions of dollars annually in foreign exchange, easing pressure on the Naira. On Tuesday, the governor of the central bank of Nigeria, Olayemi Cardoso said the country’s foreign exchange reserves has surged to over $50 billion, as foreign exchange are not frequently earmarked for fuel importations. With an export surplus of up to 20 million litres, Nigeria is poised to become the primary supplier of refined products to West and Central Africa. Under the new distribution model, the refinery will utilize its massive gantry system and a fleet of over 4,000 CNG-powered trucks to ensure products reach every corner of the country.

Nigeria slash interest rate by 50bp, joins regional policy easing trend

By: ThinkBusiness Africa The Central Bank of Nigeria (CBN) on Tuesday lowered its benchmark interest rate for the second time in five months, signaling a definitive shift toward monetary easing as the country’s inflation battle shows signs of a turning point. At the conclusion of the two-day Monetary Policy Committee (MPC) meeting in Abuja, Governor Olayemi Cardoso announced a 50 basis-point reduction in the Monetary Policy Rate (MPR), moving it from 27% to 26.5%. The decision follows a sustained decline in price pressures. According to the National Bureau of Statistics (NBS), Nigeria’s headline inflation rate eased to 15.10% in January 2026—the tenth consecutive monthly decline and the lowest level recorded since late 2020. The MPC’s “dovish” stance was also supported by a stabilizing Naira, which has gained roughly 6% against the US Dollar since the start of the year, bolstered by foreign exchange reserves that have surged toward the $49 billion mark. Joining the “African Easing Circle” Nigeria’s move aligns it with several of its continental peers who have pivoted to support economic growth now that the global inflation shock of previous years is receding. Egypt and Angola have recently cut policy rates by 100 basis points to 19% and 17.50% respectively; Kenya also slashed its rate by 25 bp to 8.75%. While countries like Ghana and Zambia have also pushed ahead with cuts, some regional giants remain cautious. The South African Reserve Bank (SARB) opted to hold its rate at 6.75% last month, choosing to wait for inflation expectations to anchor more firmly toward its 3% target. The 50 bp cut, while modest, is expected to lower borrowing costs for Nigerian businesses and potentially stimulate activity in the manufacturing and agricultural sectors. However, Governor Cardoso maintained a note of caution, stating that future decisions remain strictly “data-driven.” “While we are encouraged by the disinflationary trend, the committee remains vigilant,” Cardoso said. “Our priority is to ensure that this easing does not trigger a reversal in the hard-won stability of the Naira.”

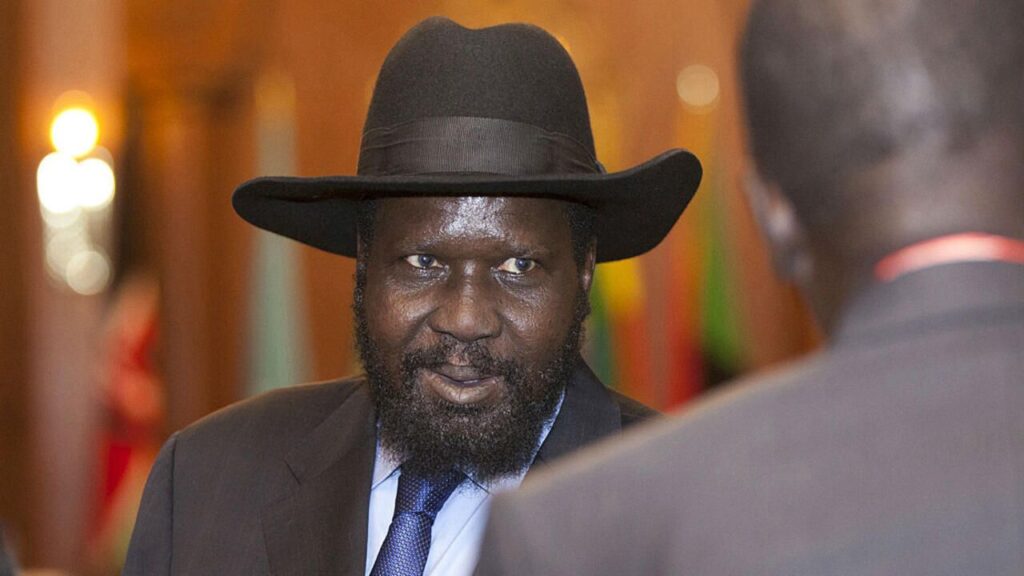

South Sudan president sacks Finance Minister after three months amid cabinet reshuffle

By: ThinkBuskness Africa President Salva Kiir of South Sudan has dismissed Finance Minister Dr. Bak Barnaba Chol after only three months in office, marking the ninth time the position has changed hands since 2020. The move, announced late Monday on state television, comes as the world’s youngest nation battles a crippling economic crisis characterized by hyperinflation and a currency in freefall. President Kiir has reappointed former finance minister Salvatore Garang Mabiordit to lead the Ministry of Finance. Garang is a veteran of Juba’s revolving-door cabinet, having previously served as Finance Minister from 2018 to 2020 and briefly again in 2023. During his previous tenures, Garang faced intense scrutiny over fiscal management, though his supporters point to his deep institutional knowledge of the country’s oil-dependent economy. The presidential decree did not stop at the Finance Ministry. In an apparent attempt to centralize control over dwindling state coffers, the President also fired the National Revenue Authority Commissioner (NRA). The dismissals come at a time of extreme hardship for South Sudanese citizens. The South Sudanese pound has lost approximately 50% of its value against the US dollar in the first two months of 2026 alone. The ongoing conflict in neighboring Sudan has severely hampered South Sudan’s ability to export crude oil—the lifeblood of its national budget, this the primary reason fueling economic pressure in the East African nation. Civil servants and members of the security forces have reportedly gone without pay for over six months, leading to fears of social unrest and a further breakdown in public services. No reason was given for the dismissal of the former finance minister.

AfDB and UNDP target $1 trillion GDP boost via new AI 10 Billion Initiative

By: ThinkBusiness Africa The African Development Bank Group (AfDB) and the United Nations Development Programme (UNDP) have officially launched the AI 10 Billion Initiative, a landmark continental drive designed to transform Africa from a consumer of technology into a global leader in responsible Artificial Intelligence. According to a press statement from AfDB on Monday, the initiative was launched during the Nairobi AI Forum 2026, where government leaders, tech innovators, and private sector giants gathered to chart a course for Africa’s digital sovereignty. The initiative is a response to the AfDB’s June 2025 flagship report, which projected that AI could add $1 trillion to Africa’s GDP by 2035. To capture this value, the new partnership aims to mobilize $10 billion in blended finance over the next decade. The program focuses on high-impact sectors where AI can bridge traditional development gaps: As an immediate outcome of the forum, the initiative has already committed to providing 1.5 million GPU hours to 130 African innovators. Additionally, a new Cybersecurity Readiness Initiative was launched in partnership with Cisco to ensure that Africa’s burgeoning digital infrastructure remains secure by design. The AfDB and UNDP will now begin a multi-country roadshow to secure further commitments from G7 partners and private equity firms, aiming to turn the “Nairobi Momentum” into a permanent shift in the global tech landscape.

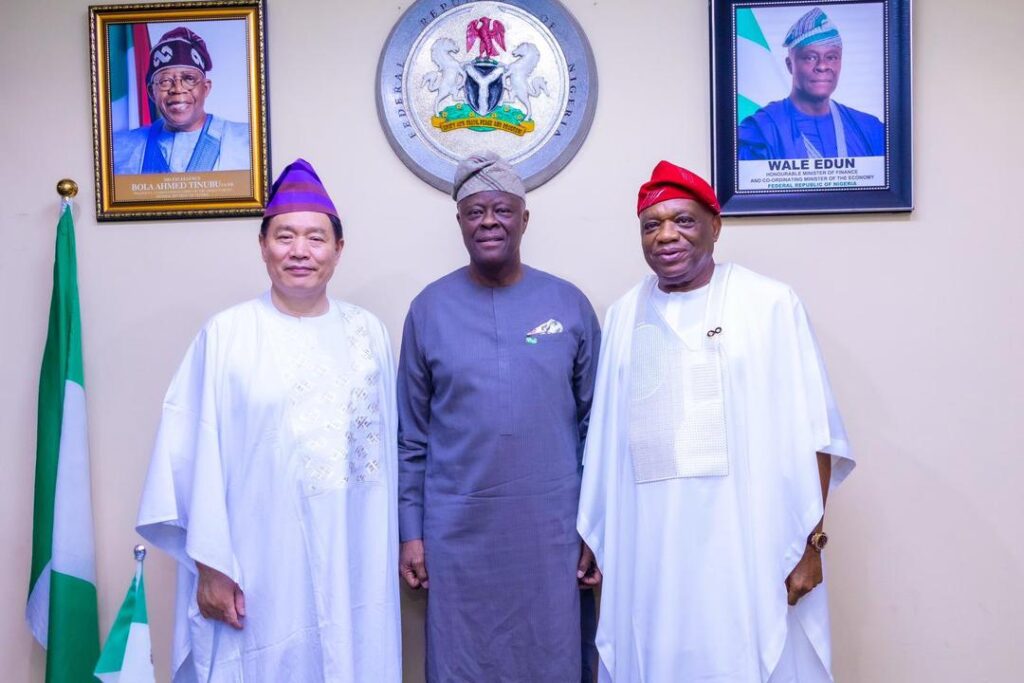

Nigeria eyes $5.7bn FDI, finance minister meets Chinese energy giants over power and mining

By: ThinkBusiness Africa The Nigerian Government has taken a decisive step toward closing the country’s infrastructure gap, advancing negotiations for a landmark $5.7 billion investment package with China’s GCL Group. A post on X (Twitter) from the Ministry of Finance, confirmed the Honourable Minister of Finance and Coordinating Minister of the Economy, Wale Edun, received a high-level delegation from the Chinese energy conglomerate in Abuja on Monday. The talks, facilitated by Senator Orji Uzor Kalu,Chairman of Swiber Africa, GCL’s local partner in the ambitious venture signify a major push to attract foreign direct investment (FDI) into the nation’s power, mining, and manufacturing sectors. The $5.7 billion proposal is designed to address Nigeria’s most pressing economic bottlenecks—specifically energy deficits and the lack of domestic value addition in the solid minerals sector. In January, GCL and Swiber Africa signed a New Energy Industry Framework Cooperation Agreement to solve Nigeria’s energy problems through development of a new-generation power system and the lithium battery industry chain. The Finance Ministry noted that the scale of this investment is a direct result of the economic reforms initiated under President Bola Ahmed Tinubu. Minister Wale Edun emphasized that these reforms are creating a predictable and investor-friendly environment, essential for securing long-term capital. “This engagement reflects rising investor confidence in the reforms under President Bola Ahmed Tinubu,” the Ministry of Finance stated. “It supports Nigeria’s strategic shift from raw exports to domestic production.” The GCL Group, a global leader in clean energy and industrial technology, brings technical expertise that could transform Nigeria’s mining landscape—specifically in the lithium battery value chain.

Nigeria defeats European tech giant in $6.2M international arbitration

By: ThinkBusiness Africa The Federal Government of Nigeria has secured a landmark legal victory against European Dynamics UK Ltd, dismissing a $6.2 million (N9.3 billion) claim following a protracted international arbitration over a stalled national e-procurement project, Presidency said on Sunday. According to a statement from Bayo Onanuga, presidential spokesman, the final ruling, which is not subject to appeal, marks a significant shift in how Nigeria handles high-stakes technology disputes. The dispute originated from a contract for a World Bank-supported electronic Government Procurement (eGP) system. The tribunal’s decision centered on three critical failures by the contractor: The Bureau of Public Procurement (BPP) identified “significant functional deficiencies” during testing. The tribunal ruled that in software contracts, delivery is only valid if the system performs according to statutory requirements. As the technical expert, the contractor bore the sole obligation to ensure the system worked, regardless of any prior approvals of technical documents by the BPP. The contractor attempted to merge multiple payment phases into one. The tribunal found no evidence the BPP consented to this, ruling that it “distorted” the contractual framework. Dr. Adebowale Adedokun, Director-General of the BPP, noted that this specific vendor had previously won similar cases against various African countries. “Nigeria is the first to defeat them,” Adedokun stated. “We stood our ground because we believed in the expertise of our own Nigerian legal professionals.” He said. Attorney General of the Federation, Prince Lateef Fagbemi (SAN), hailed the victory as a signal to the international community that Nigeria is strengthening its institutions and protecting national resources from “vulture” litigation.

Nigerian capital market contributes 33% to GDP, as valuation surpasses N123 trillion

By: ThinkBusiness Africa The Nigerian capital market has recorded a monumental leap in economic significance, with its contribution to the nation’s Gross Domestic Product (GDP) soaring to 33% in early 2026. Director-General of the Securities and Exchange Commission (SEC), Dr. Emomotimi Agama said on Sunday. This latest figure represents a staggering increase from the 13% recorded in April 2024, signaling a profound shift in the country’s financial landscape. Speaking at the inaugural meeting of the Capital Market Working Group on Market Liquidity in Lagos, Dr. Agama, revealed that total market capitalization has surged by 125% over the last 22 months. The market’s value climbed from approximately N55 trillion in April 2024 to a record-breaking N123.93 trillion by February 2026. The SEC chief attributed this growth to sustained macroeconomic reforms and a renewed wave of investor confidence. He emphasized that the capital market is transcending its reputation as a mere trading floor to become a critical pillar for industrialization. “The capital market is not gambling; it is the engine of national development. It finances roads, powers factories, and creates jobs,” Agama stated. “These figures are impressive, but they tell only part of the story. Our goal is to ensure this wealth translates into productive capacity for the entire nation.” He said. Despite the historic valuation, the SEC chief issued a call for caution regarding market depth. While the “headline” numbers are at an all-time high, the Commission is now pivoting its focus toward liquidity—the ease with which investors can buy and sell shares without causing drastic price swings. Current data suggests that much of the market’s N123 trillion value is concentrated in a few “heavyweight” sectors: To sustain this momentum, the SEC has inaugurated a multi-stakeholder working group tasked with: Streamlining trading and settlement cycles to match global standards; Onboarding 20 million new investors through fintech partnerships and mobile-first trading apps; and Implementing the Investments and Securities Act (ISA) 2025 to bring the thriving digital asset and cryptocurrency space under formal oversight. Last year, the Nigerian stock market moved to a shorter settlement cycle, transitioning from traditional T+3 (trade day, plus 3 business days), to T+2 (trade day, plus 2 business day) settlements. This move made the Nigerian capital market increasingly attractive to investors compared to its African counterparts who are still stuck with the traditional T+3. As the Nigerian Exchange (NGX) All-Share Index (ASI) nears the psychological barrier of 200,000 points, analysts suggest that the market is finally reflecting the true scale of Nigeria’s corporate potential. However, the SEC maintains that the journey to becoming a “global standard” will depend on making the market more inclusive for the average Nigerian citizen.