Large-scale financial reforms do not succeed solely because regulatory requirements are introduced. They succeed because financial systems possess the institutional capacity, market infrastructure, and regulatory architecture required to mobilise capital at scale.

Nigeria’s 2024–2026 banking recapitalisation exercise illustrates this distinction.

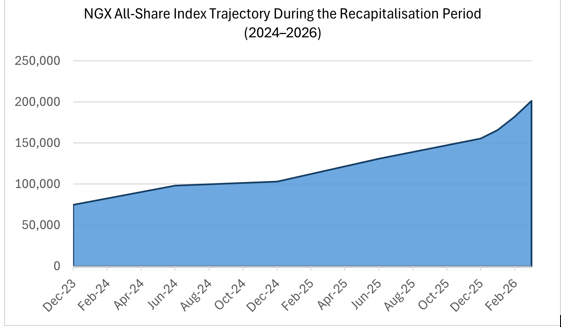

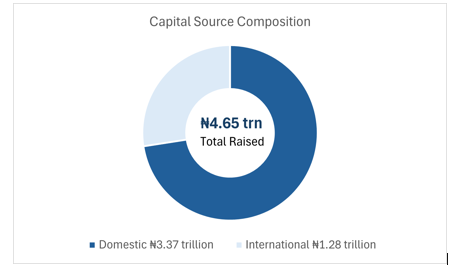

By April 2026, Nigerian banks had raised ₦4.65 trillion in fresh equity, 33 banks had fully complied with revised capital requirements, and the NGX All-Share Index reached a record 201,287 points.

The immediate story is one of successful recapitalisation. The broader story, however, is the role played by the capital market and the institutions supporting it.

Source: NGX, ABC Research, 2026

Unlike the 2005 banking consolidation, which relied heavily on mandatory mergers and regulatory pressure, the 2024–2026 exercise was largely driven by voluntary market participation. It was supported by stronger coordination among the Securities and Exchange Commission (SEC), Central Bank of Nigeria (CBN) and Nigerian Stock Exchange (NGX), improved digital issuance systems, and a regulatory framework that broadened investor participation and reduced friction across the capital formation process.

The recapitalisation therefore represents more than a banking sector milestone. It represents the strongest test yet of whether Nigeria’s capital market and regulatory institutions have matured sufficiently to support large-scale economic transformation.

This brief evaluates whether these developments reflect a lasting structural improvement in Nigeria’s capital market capacity and whether the success of the exercise can be sustained and replicated in other sectors.

THE REGULATORY LAYER: SEC, CBN, AND NGX

Nigeria’s key market institutions – the SEC, CBN, and NGX – operate at significant scale but have historically faced coordination challenges due to differing mandates. The 2024–2026 recapitalisation marked the most coordinated inter-agency execution in the market’s history, supported by the Investments and Securities Act (ISA) 2025 and the SEC’s Recapitalisation Framework introduced in June 2024.

Despite the complexity of the exercise, these institutions were central to its success. They streamlined approvals, resolved emerging structural issues, and reduced friction across the issuance process.

The SEC played a catalytic role through faster approval timelines while maintaining full disclosure standards. The CBN provided clarity on holding company structures and hybrid capital instruments, allowing banks to optimise capital structures efficiently. The NGX supported secondary market activity, contributing to strong market performance during the recapitalisation period.

Collectively, these institutions strengthened Nigeria’s financial architecture by improving liquidity, reducing approval delays, and enabling capital formation at an unprecedented scale.

Key Takeaway: The 2024–2026 exercise demonstrated what becomes possible when strong institutions operate with aligned mandates. Regulation did not simply supervise the process; it enabled it.

THE ROLE OF THE CAPITAL MARKET: FOUR FUNCTIONS DEMONSTRATED

The 2024–2026 recapitalisation shows Nigeria’s capital market evolving from a passive listing platform into core infrastructure for financing national transformation. Four key functions were clearly demonstrated.

First, it acted as a mobilisation engine, absorbing ₦4.65 trillion in equity issuance over 24 months without sustained price instability, subscription failures, or disruption in secondary trading.

Second, it served as a legitimising mechanism, where investors actively evaluated institutions before subscribing, strengthening market discipline and confidence.

Third, it functioned as an aggregation platform, pooling ₦3.37 trillion from domestic investors and ₦1.28 trillion from international investors.

Fourth, it acted as a democratisation channel, bringing approximately 500,000 new investors into the market through NGX Invest and significantly broadening participation.

Together, these functions highlight a capital market becoming increasingly central to large-scale financing and economic development.

Source: SEC Report, 2026

A PATTERN SEEN BEFORE: MARKET-MEDIATED REFORM IN COMPARABLE ECONOMIES

Nigeria’s transition mirrors patterns observed in comparable emerging economies. Following India’s 1991 liberalisation, banks strengthened capital through public market listings rather than forced mergers. Brazil followed a similar path through selective consolidation and capital market deepening.

Nigeria appears to be entering a similar transition. Tier-1 institutions have strengthened capital positions and increasingly demonstrate regional competitiveness.

However, sustained progress will depend on whether capital market development translates into broader financial deepening and improved real-sector outcomes.

Key Takeaway: Comparable economies demonstrate that large banks alone are insufficient. Strong markets and strong institutions remain central.

THE CAPITAL ALLOCATION GAP

Domestic investors accounted for ₦3.37 trillion, representing 72.55% of total capital raised, while international investors contributed ₦1.28 trillion.

This composition reflects a structural shift within Nigeria’s financial system. Unlike earlier reform cycles that depended heavily on public sector support, the 2024–2026 exercise relied primarily on private savings mobilisation.

However, Nigeria’s investment requirements remain significantly larger than current capital mobilisation levels.

The challenge therefore is increasingly not whether capital can be mobilised, but whether larger pools of long-term capital can be developed and allocated efficiently.

Source: SEC, ABC Research 2026

Key Takeaway: Domestic capital mobilisation is real and expanding, but remains relatively small compared with Nigeria’s broader investment needs.

WHAT THIS MEANS: CREDIT, JOBS, AND THE TRANSMISSION MULTIPLIER

Evidence from emerging markets suggests recapitalisation improves financial stability, credit capacity, and broader economic outcomes when supported by strong supervision and market credibility.

Nigeria possesses substantial domestic capital pools, particularly within pensions and institutional assets.

The key question therefore is no longer simply whether banks can raise capital.

The larger question is whether stronger balance sheets and deeper markets will translate into increased financing for SMEs, manufacturing, and productive sectors of the economy.

The ultimate test of recapitalisation is not capital raised, but capital transmitted.

CONCLUSION

Nigeria’s capital market is evolving from a narrow financing platform into broader infrastructure capable of supporting economic transformation.

The successful mobilisation of ₦4.65 trillion demonstrates important progress.

However, the broader lesson is institutional. Without stronger market infrastructure, coordinated institutions, and more innovative regulation, the recapitalization exercise would likely have produced materially different outcomes.

The key question is no longer whether capital can be raised. The question now is whether these gains can be sustained and translated into broader economic impact.