Nigeria’s capital market is entering one of its most significant restructuring phases in more than a decade. In January 2026, the Securities and Exchange Commission (SEC) introduced revised minimum capital requirements for capital market operators, increasing the financial thresholds by as much as 3,400% required for firms to operate across multiple market segments and setting a June 30, 2027 deadline for full compliance.

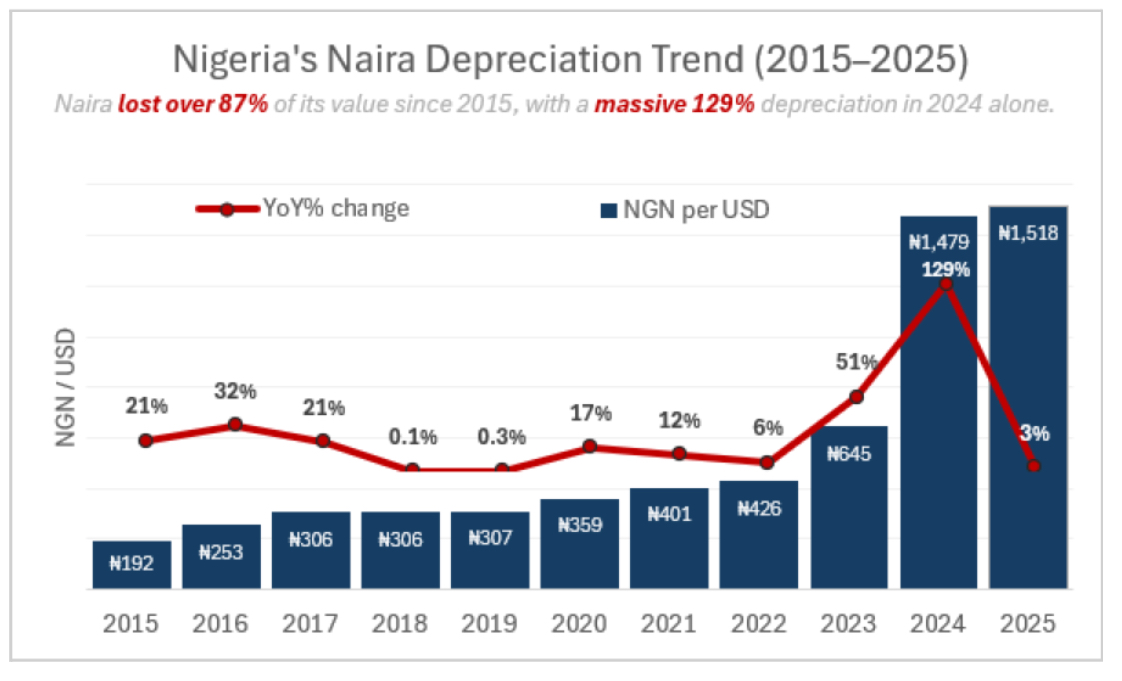

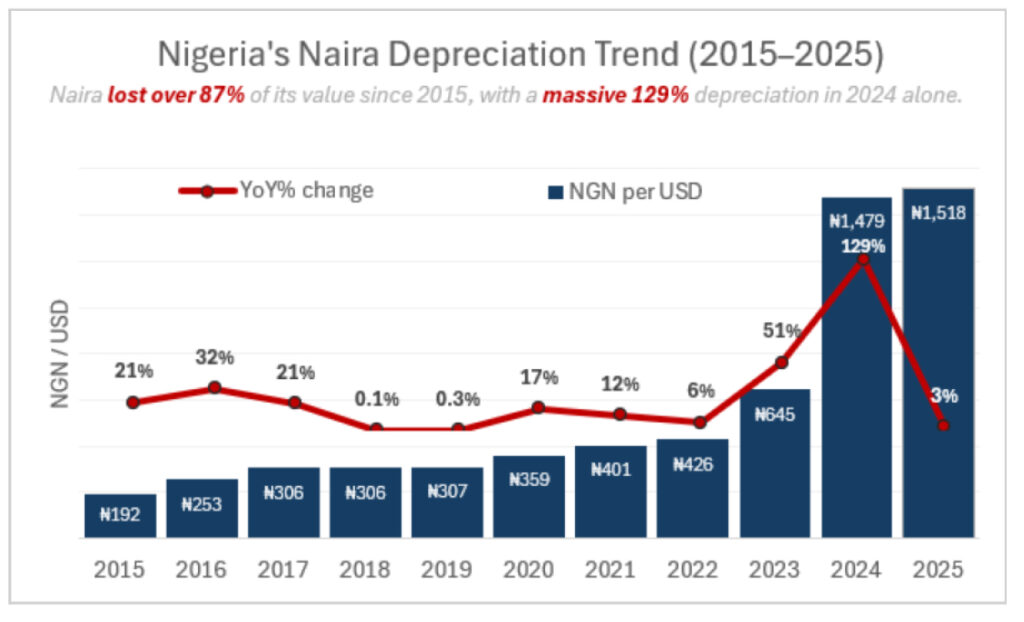

The reform comes after more than ten years of regulatory stagnation. The previous capital framework was introduced in 2015, when the naira traded at approximately ₦200 to the US dollar and Nigeria’s financial ecosystem was considerably less complex. Since then, inflation, currency depreciation, technological innovation, and the emergence of new asset classes have fundamentally altered the operating environment. Yet the minimum capital requirements governing market operators remained largely unchanged.

Source: Nigeria’s official exchange rate (Nigerian naira per US$) 2015 – 2025

Over time, this created three major challenges. First, the sharp depreciation of the naira significantly reduced the real value of existing capital thresholds, weakening their effectiveness as measures of financial strength and risk absorption capacity. Second, the framework no longer reflected the realities of a modern capital market, failing to adequately account for digital asset operators, fintech-driven investment platforms, commodity market intermediaries, and other emerging segments. Third, the industry became increasingly fragmented, with many operators possessing limited balance sheet capacity despite growing transaction volumes and market complexity.

The SEC’s recapitalisation initiative seeks to address these structural weaknesses by strengthening the financial resilience of market operators, improving investor protection, supporting larger and more sophisticated market activities, and enhancing the competitiveness of Nigeria’s capital market. The reform also aligns with broader efforts to modernise the country’s financial sector and deepen domestic capital formation at a time when Nigeria is seeking to attract greater levels of local and international investment.

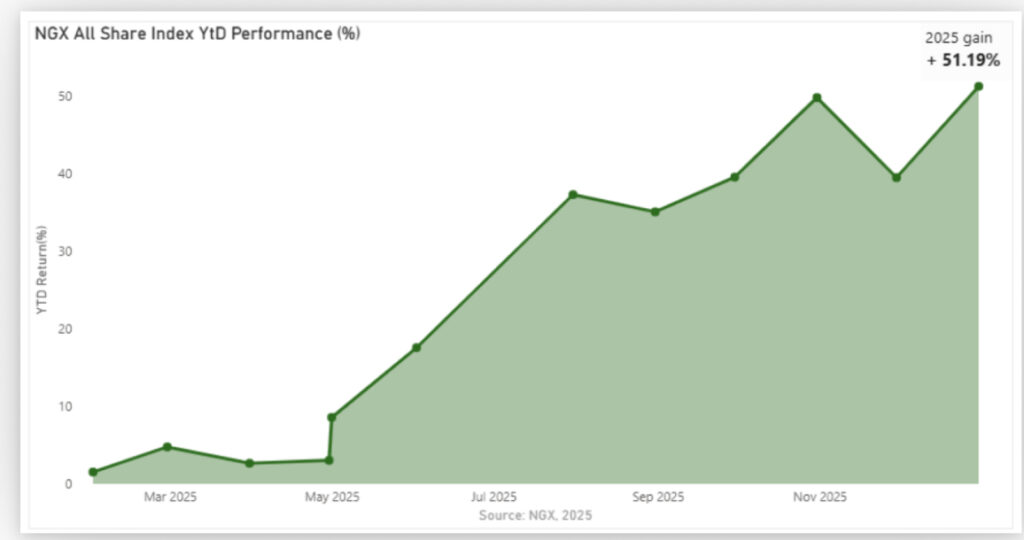

The initiative follows a wider trend of recapitalisation across Nigeria’s financial system. Between 2024 and 2026, the banking sector recapitalisation programme mobilised approximately ₦4.65 trillion in fresh equity capital and contributed to stronger market confidence, with the NGX All-Share Index reaching record highs during the period. The SEC’s reform represents a similar attempt to build stronger institutions capable of supporting long-term economic growth.

Source: NGX, 2026

This brief sets out to examine the rationale behind the SEC’s capital threshold raise, the shortcomings of the previous framework, the key changes introduced under the new regime, and the implications for market operators, investors, and the future structure of Nigeria’s capital market.

Key Takeaway: The 2015 capital framework was rendered structurally inadequate by naira depreciation, market complexity, and a fragmentation of the intermediary base that left Nigeria’s capital market unable to execute transactions at a size commensurate with the country’s economic ambitions. The January 2026 circular is a correction of accumulated distortion, not a routine review. Investors should read it as a signal that Nigeria’s regulatory posture has shifted from maintenance to transformation.

RECAPITALIZATION: A BROADER FINANCIAL SECTOR PATTERN

Nigeria’s capital market recapitalisation does not stand in isolation. It is part of a broader pattern of financial capacity strengthening across the financial system, where regulators repeatedly use capital thresholds as a structural tool to reshape institutions, improve resilience, and expand scale.

A key precedent is the 2004–2005 banking consolidation, which reduced the number of banks from over 80 to 25 after a sharp increase in minimum capital requirements. That reform fundamentally strengthened the banking system, created larger balance sheets, and enabled regional expansion across West Africa.

More recently, the 2024–2026 banking recapitalisation cycle required banks to raise substantial new equity in response to macroeconomic pressures and currency volatility. The exercise produced no institutional failures, strengthened systemic stability, and contributed to a record rally in the NGX All-Share Index, which reached 201,287 points, while also bringing in an estimated half a million new retail investors through equity issuance activity.

Against this backdrop, Nigeria is currently running three concurrent recapitalisation exercises across banking, insurance, and capital markets within a 36-month window, all aligned directly or indirectly with the broader ambition of building a $1 trillion economy. The banking exercise has already been completed, the insurance reform is ongoing, and the SEC capital market reform runs from 2026 to 2027. For investors, this is not a series of isolated reforms but a coordinated expansion of capital requirements across the entire financial intermediary system.

Key Takeaway: Nigeria’s banking, insurance, and capital market recapitalisations represent a single coordinated restructuring of the financial system within one policy cycle. For investors, the key constraint is not regulatory ambition but capital absorption capacity, as successive sectors compete for the same pool of equity funding within a compressed timeframe.

AFRICAN PRECEDENTS: HAS ANY MARKET DONE THIS BEFORE?

Nigeria is not the first African market to raise capital requirements for market operators. Kenya’s 2025 capital markets reforms introduced a tiered broker-dealer structure, increased capital thresholds across key operator categories, and extended requirements to trustees and custodians. Like Nigeria’s current exercise, the reforms were designed to strengthen institutional capacity and support market consolidation. The Kenyan experience shows how higher capital standards can be used to reshape industry structure rather than simply improve compliance.

South Africa offers a more advanced benchmark. The Financial Sector Conduct Authority operates a risk-based capital framework where requirements are linked to income, assets under management, and risk exposure rather than fixed minimums alone. The system also covers a broader range of market participants, including hedge funds and derivatives intermediaries. This demonstrates the direction many mature markets have taken as they move beyond static capital thresholds toward continuous prudential supervision

Egypt provides a cautionary example. Although capital adequacy reforms were introduced in 2021, repeated deadline extensions weakened enforcement and limited the intended consolidation of the sector. For Nigeria, this highlights that regulatory credibility is as important as policy design, particularly as operators approach the June 2027 compliance deadline.

THE NEW ARCHITECTURE: WHAT CHANGED, BY HOW MUCH, AND FOR WHOM

Tiered, Risk-Differentiated Thresholds Across Operator Categories

The most important change in the new Securities and Exchange Commission (SEC) capital framework is not only the increase in minimum capital levels, but the redesign of how capital requirements are determined across the capital market. In January 2026, the SEC replaced a long-standing uniform capital regime with a tiered, risk-based structure that links capital thresholds directly to the nature of activities, the scale of operations, and the systemic importance of each operator. This marks a clear departure from a one-size-fits-all model toward a framework that differentiates firms based on their actual risk exposure within the financial system.

Under this approach, capital is no longer assigned by licence category alone but by function and complexity. Operators with broader mandates, higher transaction exposure, or balance-sheet involvement are now required to hold significantly higher capital buffers than those with narrower roles. The intention is to ensure that financial strength is proportionate to risk, reducing the likelihood of institutional failure and limiting systemic spillovers in periods of market stress.

At the broker-dealer level, firms combining client execution and proprietary trading are now required to hold ₦2 billion in minimum capital, up from ₦300 million, a 567% increase. This reflects the higher risk created when firms manage both client transactions and their own trading positions. Fund managers overseeing assets above ₦20 billion must now maintain ₦5 billion in capital, compared to the previous flat requirement of ₦150 million, representing a 3,233% increase and introducing a direct link between scale and prudential buffers.

At the infrastructure level, the Central Securities Depository is now subject to a ₦15 billion minimum capital requirement, establishing a formal capital floor for a systemically critical institution. Within brokerage, a three-tier structure applies: client execution brokers (₦600 million), proprietary traders (₦1 billion), and full broker-dealers (₦2 billion), reflecting increasing risk with expanded activity scope.

The framework also extends regulation to emerging segments for the first time, including digital sub-brokers (₦100 million) and other fintech and virtual asset operators under proportionate capital rules. Securities exchanges and central counterparties are each required to hold ₦10 billion, reinforcing the stability of core market infrastructure.

Table 1: Revised Minimum Capital Thresholds — Key Operator Categories

| Operator Category | Old Minimum (₦) | New Minimum (₦) | Change (%) |

| Broker (Client Execution Only) | 200 million | 600 million | +200% |

| Dealer (Proprietary Trading Only) | 100 million | 1 billion | +900% |

| Broker-Dealer (Combined) | 300 million | 2 billion | +567% |

| Fund Manager — Full Scope (AUM >₦20bn) | 150 million | 5 billion | +3,233% |

| Fund Manager — Limited Scope | 150 million | 2 billion | +1,233% |

| Issuing House / Investment Bank | 150 million | 5 billion | +3,233% |

| Asset Manager / Custodian | 150 million | 3 billion | +1,900% |

| Venture Capital Fund Manager | 20 million | 200 million | +900% |

| Digital Sub-Broker | None | 100 million | New |

| Securities Exchange (Composite) | 1 billion* | 10 billion | +900% |

| Central Securities Depository | None specified | 15 billion | New |

Source: SEC Nigeria, (March 18, 2026).

Key Takeaway: The SEC has replaced flat capital thresholds with a risk-tiered system that scales financial requirements based on activity, complexity, and systemic importance, fundamentally redefining capital adequacy in Nigeria’s market.

THE CONSOLIDATION ARITHMETIC: WHO SURVIVES, WHO EXITS

From 200 Dealing Firms to a Restructured Intermediary Ecosystem

One of the key determinants of survival in the recapitalisation exercise is access to capital. While all operators face higher minimum requirements, not all firms can raise fresh equity within the compliance window, making capital access the primary filter for survival and scale.

Nigeria’s capital market currently has about 200 dealing firms, over 30 fund managers, and a wide range of licensed intermediaries, most built under the 2015 framework that enabled low entry capital and produced a fragmented market. A key structural divide now emerges between standalone firms and those embedded within financial holding structures. Nigeria’s largest capital market operators sit within banking groups under the Central Bank of Nigeria’s Financial Holding Company framework, including GTCO, Stanbic IBTC, Access Holdings, FBN Holdings, and UBA. This structure allows capital to be mobilised at group level, giving bank-backed intermediaries a clear advantage in meeting SEC thresholds and positioning them as natural consolidators.

In contrast, independent operators rely on retained earnings, private investors, or strategic partnerships, all of which are tightening as multiple sectors compete for the same pool of capital. As a result, funding pressure is widening the gap between group-backed firms and standalone intermediaries.

Consequently, the higher capital thresholds create strong consolidation pressure ahead of the June 2027 deadline. Many mid-tier and smaller firms will struggle to raise capital independently, making mergers, acquisitions, or licence downgrades the most likely outcomes and reducing the industry to fewer but stronger intermediaries.

Ultimately, the Investments and Securities Act 2025 signals a managed consolidation process rather than disorderly exits, echoing Nigeria’s banking recapitalisation experience.

Key Takeaway: The capital increases make consolidation unavoidable. Borrowed funds are excluded from qualifying capital, so firms must merge, be acquired, or exit certain functions. The result will be fewer intermediaries, but stronger, better-capitalised institutions with higher long-term earning power.

REGIONAL BENCHMARKS: CLOSING A STRUCTURAL GAP

Nigeria’s New Thresholds in Continental and Global Context

In regional and global context, the revised Securities and Exchange Commission (SEC) capital framework addresses a long-standing structural gap in Nigeria’s capital market. For over a decade, Nigeria’s capital thresholds remained relatively low compared to global markets, limiting the ability of domestic intermediaries to compete for large mandates, execute cross-border transactions, or position themselves as credible counterparts to international investment banks and asset managers.

In Kenya, the Capital Markets Authority requires approximately KES 1 billion (about ₦9.5 billion) for investment banks and around KES 100 million (about ₦950 million) for stockbrokers. Despite Nigeria having a significantly larger economy and deeper financial system, its previous requirements stood at about ₦150 million for issuing houses and ₦300 million for broker-dealers. This created a structural imbalance where Nigerian firms were often undercapitalised relative to their market ambitions, forcing reliance on foreign or regional institutions for larger transactions.

South Africa operates a more advanced system under the Financial Sector Conduct Authority, combining base capital requirements with ongoing solvency rules tied to assets and income. The United Kingdom goes further with a dynamic model under the FCA’s K-Factor framework, where capital is linked to client exposure, assets under management, and counterparty risk rather than fixed thresholds.

Nigeria’s new framework remains simpler and uses fixed minimum capital levels, but it significantly narrows the regional gap. The ₦2 billion broker-dealer requirement (≈ $1.3 million), ₦5 billion issuing house threshold (≈ $3.3 million), and ₦15 billion requirement for the Central Securities Depository bring key institutions closer to international expectations, particularly at the infrastructure level.

| Market | Regulator | Broker-Dealer / Equivalent | Structure Type |

| Nigeria | SEC | ₦2 billion (combined broker-dealer) | Fixed, tiered risk-based |

| Kenya | Capital Markets Authority | KES 100m stockbrokers | Fixed, incremental |

| South Africa | FSCA | Risk-based capital adequacy | Dynamic risk-based |

Overall, Nigeria now sits above most East African broker-level thresholds, below South Africa and the UK at the upper end of sophistication, but within a credible international range for investment banking and market infrastructure functions. The key change is structural from undercapitalisation that constrained scale to a framework that now supports larger transactions and stronger regional competitiveness.

Key Takeaway: Nigeria’s capital thresholds do not yet match advanced global markets, but they close a major regional gap and reposition local intermediaries for credible participation in larger regional and cross-border transactions.

MARKET IMPLICATIONS: WHO GAINS, WHO ADJUSTS, AND WHAT CHANGES

The impact of the reform will vary across operators, creating a clear split between large institutions and smaller firms. Large intermediaries are better positioned due to stronger access to capital, institutional backing, and diversified revenues. For them, the new requirements are less about survival and more about consolidation and expansion, with opportunities to increase market share and pursue acquisitions.

Smaller operators face tighter conditions as higher capital thresholds and weaker fundraising environments make compliance more difficult. This creates a dual-speed market where larger firms gain strength while smaller firms must scale, specialise, merge, or restructure to remain viable. Survival will depend less on size alone and more on the ability to attract capital and adapt business models.

The recapitalisation cycle is expected to follow a banking-style pattern, with private placements and strategic investors driving most capital raises between 2026 and 2027. Because most operators are unlisted, funding will be concentrated in private and institutional channels, increasing ownership concentration.

For issuers, the market will move toward fewer but stronger intermediaries, improving execution quality, underwriting capacity, and transaction reliability, even as relationship diversity reduces. For international investors, stronger capital standards improve confidence in counterparties and reduce perceived market risk.

The transition will be costly in the short term, with higher compliance and restructuring expenses, but it delivers a longer-term gain in stability, efficiency, and market depth.

Key Takeaway: The recapitalisation is a structural reform, not just a capital increase. It will reduce the number of intermediaries but produce stronger, better-governed institutions capable of handling large, institutional-scale transactions. For long-term investors, the signal is clear as the market is becoming more resilient and is positioning itself for deeper equity and debt activity, as well as stronger cross-border investment flows under AfCFTA.