Nigeria’s Banking Recapitalisation: The Role of Capital Markets Revisited

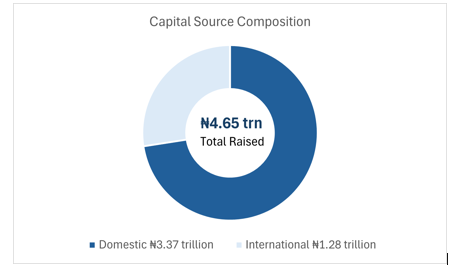

Large-scale financial reforms do not succeed solely because regulatory requirements are introduced. They succeed because financial systems possess the institutional capacity, market infrastructure, and regulatory architecture required to mobilise capital at scale. Nigeria’s 2024–2026 banking recapitalisation exercise illustrates this distinction. By April 2026, Nigerian banks had raised ₦4.65 trillion in fresh equity, 33 banks had fully complied with revised capital requirements, and the NGX All-Share Index reached a record 201,287 points. The immediate story is one of successful recapitalisation. The broader story, however, is the role played by the capital market and the institutions supporting it. Source: NGX, ABC Research, 2026 Unlike the 2005 banking consolidation, which relied heavily on mandatory mergers and regulatory pressure, the 2024–2026 exercise was largely driven by voluntary market participation. It was supported by stronger coordination among the Securities and Exchange Commission (SEC), Central Bank of Nigeria (CBN) and Nigerian Stock Exchange (NGX), improved digital issuance systems, and a regulatory framework that broadened investor participation and reduced friction across the capital formation process. The recapitalisation therefore represents more than a banking sector milestone. It represents the strongest test yet of whether Nigeria’s capital market and regulatory institutions have matured sufficiently to support large-scale economic transformation. This brief evaluates whether these developments reflect a lasting structural improvement in Nigeria’s capital market capacity and whether the success of the exercise can be sustained and replicated in other sectors. THE REGULATORY LAYER: SEC, CBN, AND NGX Nigeria’s key market institutions – the SEC, CBN, and NGX – operate at significant scale but have historically faced coordination challenges due to differing mandates. The 2024–2026 recapitalisation marked the most coordinated inter-agency execution in the market’s history, supported by the Investments and Securities Act (ISA) 2025 and the SEC’s Recapitalisation Framework introduced in June 2024. Despite the complexity of the exercise, these institutions were central to its success. They streamlined approvals, resolved emerging structural issues, and reduced friction across the issuance process. The SEC played a catalytic role through faster approval timelines while maintaining full disclosure standards. The CBN provided clarity on holding company structures and hybrid capital instruments, allowing banks to optimise capital structures efficiently. The NGX supported secondary market activity, contributing to strong market performance during the recapitalisation period. Collectively, these institutions strengthened Nigeria’s financial architecture by improving liquidity, reducing approval delays, and enabling capital formation at an unprecedented scale. Key Takeaway: The 2024–2026 exercise demonstrated what becomes possible when strong institutions operate with aligned mandates. Regulation did not simply supervise the process; it enabled it. THE ROLE OF THE CAPITAL MARKET: FOUR FUNCTIONS DEMONSTRATED The 2024–2026 recapitalisation shows Nigeria’s capital market evolving from a passive listing platform into core infrastructure for financing national transformation. Four key functions were clearly demonstrated. First, it acted as a mobilisation engine, absorbing ₦4.65 trillion in equity issuance over 24 months without sustained price instability, subscription failures, or disruption in secondary trading. Second, it served as a legitimising mechanism, where investors actively evaluated institutions before subscribing, strengthening market discipline and confidence. Third, it functioned as an aggregation platform, pooling ₦3.37 trillion from domestic investors and ₦1.28 trillion from international investors. Fourth, it acted as a democratisation channel, bringing approximately 500,000 new investors into the market through NGX Invest and significantly broadening participation. Together, these functions highlight a capital market becoming increasingly central to large-scale financing and economic development. Source: SEC Report, 2026 A PATTERN SEEN BEFORE: MARKET-MEDIATED REFORM IN COMPARABLE ECONOMIES Nigeria’s transition mirrors patterns observed in comparable emerging economies. Following India’s 1991 liberalisation, banks strengthened capital through public market listings rather than forced mergers. Brazil followed a similar path through selective consolidation and capital market deepening. Nigeria appears to be entering a similar transition. Tier-1 institutions have strengthened capital positions and increasingly demonstrate regional competitiveness. However, sustained progress will depend on whether capital market development translates into broader financial deepening and improved real-sector outcomes. Key Takeaway: Comparable economies demonstrate that large banks alone are insufficient. Strong markets and strong institutions remain central. THE CAPITAL ALLOCATION GAP Domestic investors accounted for ₦3.37 trillion, representing 72.55% of total capital raised, while international investors contributed ₦1.28 trillion. This composition reflects a structural shift within Nigeria’s financial system. Unlike earlier reform cycles that depended heavily on public sector support, the 2024–2026 exercise relied primarily on private savings mobilisation. However, Nigeria’s investment requirements remain significantly larger than current capital mobilisation levels. The challenge therefore is increasingly not whether capital can be mobilised, but whether larger pools of long-term capital can be developed and allocated efficiently. Source: SEC, ABC Research 2026 Key Takeaway: Domestic capital mobilisation is real and expanding, but remains relatively small compared with Nigeria’s broader investment needs. WHAT THIS MEANS: CREDIT, JOBS, AND THE TRANSMISSION MULTIPLIER Evidence from emerging markets suggests recapitalisation improves financial stability, credit capacity, and broader economic outcomes when supported by strong supervision and market credibility. Nigeria possesses substantial domestic capital pools, particularly within pensions and institutional assets. The key question therefore is no longer simply whether banks can raise capital. The larger question is whether stronger balance sheets and deeper markets will translate into increased financing for SMEs, manufacturing, and productive sectors of the economy. The ultimate test of recapitalisation is not capital raised, but capital transmitted. CONCLUSION Nigeria’s capital market is evolving from a narrow financing platform into broader infrastructure capable of supporting economic transformation. The successful mobilisation of ₦4.65 trillion demonstrates important progress. However, the broader lesson is institutional. Without stronger market infrastructure, coordinated institutions, and more innovative regulation, the recapitalization exercise would likely have produced materially different outcomes. The key question is no longer whether capital can be raised. The question now is whether these gains can be sustained and translated into broader economic impact.

The $348 Billion Reset: What China’s Zero-Tariff Policy Means for African Investors

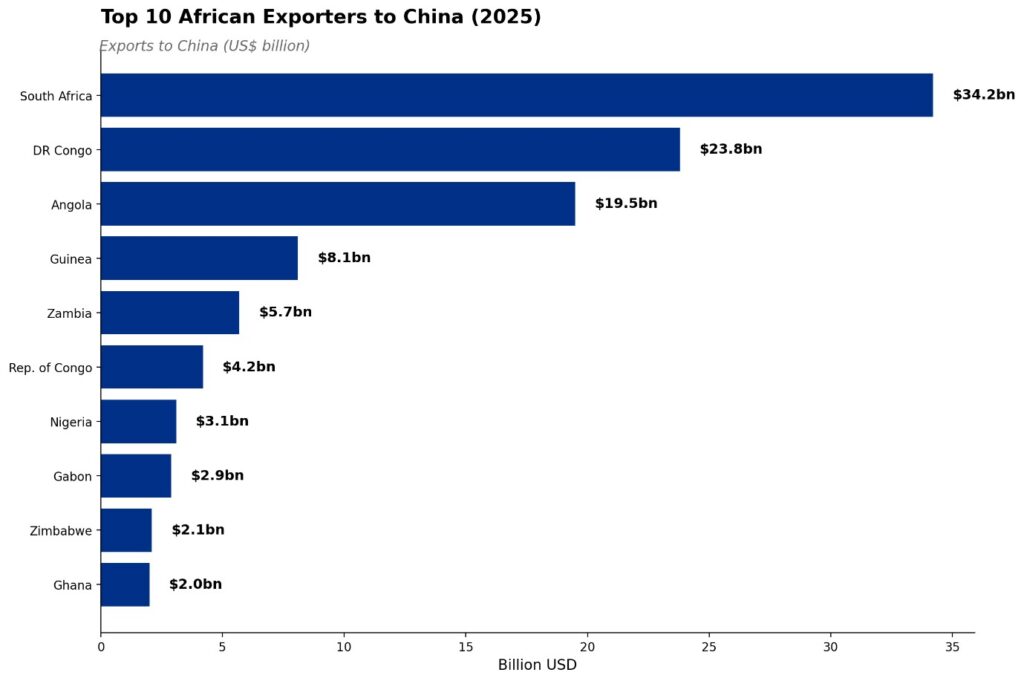

China has opened its market to all 53 African nations with diplomatic ties. The focus has shifted to which countries and industries will be the first to capitalize on the opportunity. On 1 May 2026, China implemented a historic zero-tariff policy covering 100 percent of tariff lines for all 53 African nations with diplomatic ties. The policy is locked in through April 2028, marking the first time a major economy has offered duty-free access at this scale unilaterally. Bilateral trade reached $348 billion in 2025, up 17.7% year-on-year, with Q1 2026 data showing an additional 23.7% surge. Chinese direct investment in Africa also rose 44% in early 2026, as capital shift toward processing capacity to capture returns from the duty-free trade regime. This reflects a structural reallocation of investment ahead of trade, as firms position to benefit from expanded market access within the limited policy window. Fig 1: China-Africa Trade Growth, UNcomtrade data, 2025 This latest Africa investment brief analyzes the policy’s sectoral winners, structural risks, and investment implications for African markets. I. Policy Architecture: The 2028 Horizon This initiative expands the 2024 framework for Least Developed Countries (LDCs) to major African economies including South Africa, Nigeria, and Egypt. Crucially, the rates are guaranteed only through April 2028, aligning with the broader 15th Five-Year Plan. This creates a deliberate sense of urgency for exporters to qualify and for investors to deploy capital. To support this, China has introduced “green channels” for agriculture and new direct shipping routes to compress logistics costs. Fig 2: Top 10 African Exporters to China, UNcomtrade data, 2025 Key Takeaway: This is a time-bound trade window, not a permanent regime. Investment strategies must account for a potential reversion after 2028. II. The Long Arc: How China’s Africa Trade Policy Has Evolved China has been Africa’s largest trading partner for 16 consecutive years. The May 2026 announcement is the endpoint of a 25-year progression through three distinct phases. The first phase, running from the 1990s to 2012, was driven by China’s “Go Out” policy and focused on securing oil, copper, cobalt, and bauxite while opening African markets to low-cost Chinese manufactures. The second phase began in 2013 with the launch of the Belt and Road Initiative, which shifted the relationship from transactional commodity flows to structural integration through industrial parks, special economic zones, and supply chain financing The third phase, from 2014 onward, marks a shift from state-led lending to market-driven integration under tighter financial discipline. After years of volatile policy-bank exposure and rising debt concerns, China has reduced reliance on large-scale concessional financing. Instead, the focus is on trade access, industrial participation, and private-sector expansion. The May 2026 zero-tariff policy is the centrepiece of this phase, replacing capital-heavy engagement with broader market integration and enabling Chinese firms to compete more directly across African value chains. Key Takeaway: The strategy has evolved from “building the road” through massive state debt to “using the road” via private-sector trade and digital integration. III. Chine-Africa Changing Trade Dynamics bet Since 2000, trade between Africa and China has expanded 30-fold, but the relationship is now being reshaped by three major phases. First, Africa’s exports are becoming more diversified. Hydrocarbons and raw minerals made up 85% of exports in 2005, but their share fell to under 70% by 2025. Second, Chinese exports to Africa are moving up the value chain. Electric vehicles, solar equipment, and industrial machinery helped drive Chinese exports to the continent to $225 billion in 2025. Third, the bilateral trade deficit reached a record $102 billion last year. However, because total trade between both sides grew even faster, the deficit accounted for a smaller share of overall trade than in previous years. Key Takeaway: The deficit is widening. The zero-tariff window is Africa’s most concentrated opportunity to narrow that gap by shifting from raw commodities to processed exports rather than just increasing volume. IV. Regional Divergence: Africa Is Moving at Different Speeds Africa’s economic relationship with China is not uniform. Each region is benefiting in different ways and at different speeds. Southern Africa is the continent’s leading export bloc. South Africa exported $34.2 billion to China in 2025 about 28% of Africa’s total exports driven by a diversified mix of minerals, agriculture, and processed goods. South Africa and Zimbabwe are positioned for strong near-term gains. Central Africa remains resource-driven. The DRC, Angola, and the Republic of Congo exported roughly $47 billion combined, largely through copper, cobalt, and crude oil. The next opportunity is local mineral processing and battery-material production. West Africa has the biggest untapped potential. Nigeria and Ghana underperform relative to their economic size due to oil dependence and limited processing capacity. Expanding local processing could unlock major export growth. East Africa is the fastest-growing region by percentage. Kenya, Ethiopia, Tanzania, and Rwanda are expanding exports of coffee, tea, flowers, avocado oil, and apparel, positioning the region as a rising agricultural trade corridor. North Africa is emerging as a manufacturing platform. Morocco is building an EV supply chain, while Egypt is expanding textiles and processed goods production, supported by growing Chinese industrial investment. Key Takeaway: Southern Africa captures margin; East Africa captures volume; West Africa requires investment to realize uplift. Investors must construct regionally-differentiated theses. V. Sectoral Winners: Where the Margin Lives Sectors where Chinese tariffs were previously highest capture the largest immediate gain. Agribusiness leads. Cocoa, coffee, avocado oil, citrus, wine, cashews, and dried chilli previously faced Chinese tariffs of 8 to 30 percent. At zero, they are immediately price-competitive against Southeast Asian and Latin American suppliers in one of the world’s fastest-growing premium food markets. Beyond agriculture, Namibian lobster and Tanzanian crab now compete directly with Asian suppliers. Furthermore, the policy incentivizes in-country processing for battery minerals in Zimbabwe and the DRC, allowing these nations to export value-added materials at zero tariff. Manufacturing hubs in Egypt and Morocco are also scaling to leverage zero-cost export access for finished goods. Sector Key Products Previous Tariff → 0% Agri-Processing Cocoa (Ghana/Côte d’Ivoire), Coffee (Ethiopia/Kenya), Avocados (Kenya), Chilli

Africa Invest Brief: The Strait of Hormuz and the Markets of Africa

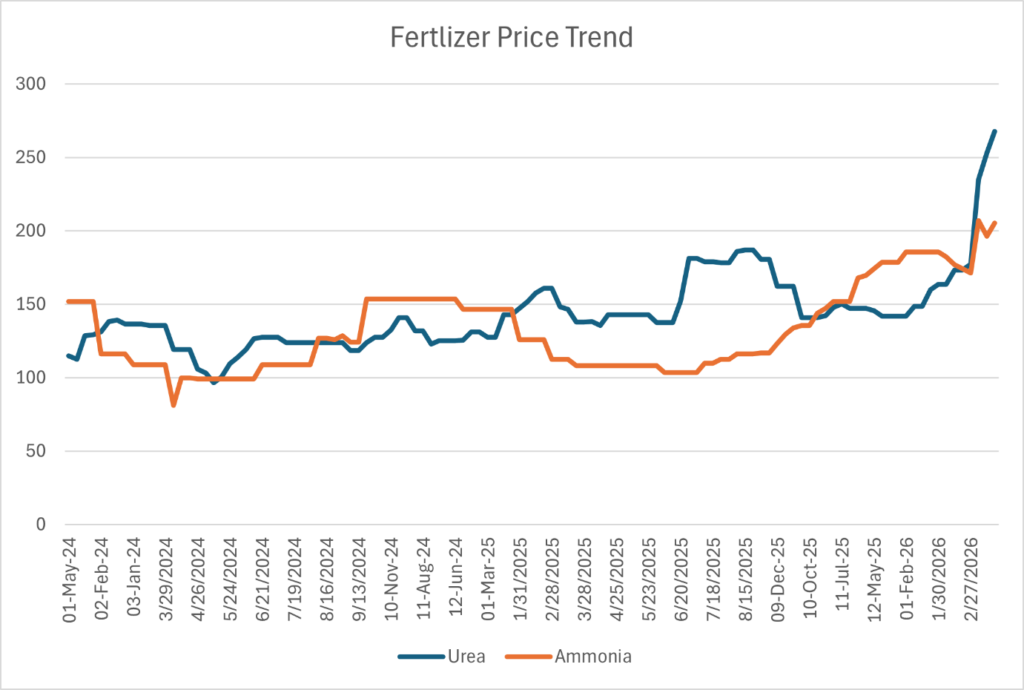

Africa and the global economy is experiencing another shock. This follows the growing and volatile US, Israel, and Iran conflict that started on the 28th of February 2026. This report provides the latest on Africa markets and investment landscape, covering key developments across equities, currencies, commodities, and capital flows between in the first quarter of the 2026. This edition highlights major macroeconomic and market trends shaping Africa’s investment outlook, as well as regional performance across financial markets. It also examines commodity movements and capital allocation patterns influencing growth and investor sentiment across the continent. A dedicated spotlight on Nigeria’s evolving tax landscape outlines the implications for both domestic and foreign investors, making it essential reading for those with exposure to Africa’s largest economy. Special Report: The Strait of Hormuz Crisis A distant war compounding crisis for households and businesses in Africa The Strait of Hormuz shock is not just a distant geopolitical event for Africa; it is an immediate economic transmission channel. From fuel prices to food costs, the effects are already filtering through the continent’s most vulnerable pressure points. The Strait handles roughly one-fifth of global oil trade and a significant share of fertilizer exports. As tensions escalated in late Q1, oil prices rose, and supply chains tightened, triggering a chain reaction across African economies. Fig 1: Brent crude oil price movement since 28 February 2026. Source: World Bank, 2026 What this means for Africa For oil exporters such as Nigeria and Angola, higher crude prices support export revenues, fiscal balances, and foreign exchange inflows. But the broader continental picture is less favourable. Nearly two-thirds of Sub-Saharan Africa’s GDP comes from net fuel-importing economies, where rising oil prices feed directly into price pressures and inflation. Higher fuel costs increase transport fares, raise business operating expenses, and push up food prices in urban markets. For households, this shows up as a widening cost-of-living squeeze. Key Takeaway: The Strait of Hormuz crisis is a dual-speed shock. Oil exporters benefit from higher prices, but most African economies, being net importers, face rising inflation, currency pressure, and growing food security risks. For households, the impact is clear: higher costs today, and potential food price increases ahead. The fertilizer story: Africa’s hidden vulnerability Fertilizer markets present an additional risk. Around 30% of globally traded fertilizer, urea, and ammonia transits the Strait, with the Gulf supplying a large share of global exports. Disruptions have pushed urea prices up by as much as 50% (IFRI, 2026) during the critical March-to-May planting season. This reflects the disruption to roughly one-third of the global fertilizer trade. Farmers are adjusting usage, increasing the likelihood of weaker harvests and higher food prices later in the year. Fig 2: Source: Bloomberg, ABC Research 2026 Currency pressures are compounding the effect. Higher import bills are driving demand for foreign exchange, weakening local currencies and reinforcing inflation across fuel, food, and other imports. Key Takeaway: The fertilizer crisis is arriving at the worst possible time, the March–May planting season. Farmers who miss this window face harvest shortfalls that translate into food price inflation in September–October 2026, then currency pressure, then further inflation. For investors in African consumer goods, FMCG, and agricultural stocks, this is a near-term earnings risk to model now, not when the data arrives in Q3. The Africa Market Snapshot Africa opens 2026 on a bull run While global indices struggled under the weight of rising Middle East tensions and oil price spikes in late March, the S&P 500 fell roughly 1.7% in the final week of the quarter. African stock markets were experiencing all-time highs, cutting interest rates, and currencies strengthened. The continent did not move as one, but the direction was unmistakably positive. Fifteen African central banks held monetary policy meetings in the first two months of the year. Eight of them cut rates, including Kenya, Egypt, Angola, Ghana, Mozambique, Zambia, Nigeria, and the Democratic Republic of Congo. This easing wave signals something important: after more than two years of aggressive rate hikes to fight post-pandemic inflation, African policymakers now have enough confidence to start putting growth back on the agenda. Inflation has cooled meaningfully in several countries.In Kenya, headline inflation fell to approximately 3.5% by early 2026, well within the Central Bank of Kenya’s 2.5–7.5% target band. Ghana’s inflation declined to 12.1% in July 2025 (its lowest since December 2021) and continued moderating into 2026 despite the Bank of Ghana’s aggressive easing.. In Zimbabwe, inflation has fallen sharply from its 2024 highs following ZiG currency reforms. In Zambia, easing inflation gave the Bank of Zambia room to cut rates by 75 basis points to 13.5% in Q1 2026. At the same time, African startup ecosystems raised $487.25 million in the first two months of 2026, an 11% increase over the same period in 2025. The composition of that money is shifting, though. Equity capital fell significantly, while debt financing more than doubled. Investors are becoming more selective and more structured. The era of easy venture money may be fading, but the demand for African solutions is not. Key Takeaway: Africa entered 2026 with easing monetary policy, strengthening currencies across most major markets, record equity performance on its largest exchange, and a maturing startup ecosystem. The opportunity is real, but so is the need to be selective. Equities Nigeria: The NGX crosses 200,000 points, a historic first Fig 3: The NGX All Share Index Trend The Nigerian Exchange All-Share Index delivered the most dramatic equity story on the continent in Q1 2026. It started the year at 155,613 points and never looked back. The rally was broad-based. Banking, consumer goods, industrials, and insurance all contributed. Foreign portfolio investors returned in force, with $3 billion in inflows recorded in January alone. What is fuelling this? A combination of falling inflation, a more stable naira, CBN monetary easing (benchmark rate cut 50bps to 27%), banking sector recapitalisation, and growing confidence in Nigeria’s macro direction. Key Takeaway: The NGX has delivered over 29% in year-to-date returns through late March. Those who