Nigeria moves to protect banks with strict limits on affiliate exposure

LAGOS – The Central Bank of Nigeria (CBN) has proposed strict limits on loans, asset transfers, and financial exposures between banks and their affiliates to prevent financial distress from spreading across corporate banking groups. Under the new draft guidelines, banking subsidiaries are prohibited from extending credit or guaranteeing obligations of closely linked entities, including financial holding companies, without prior written approval from the apex bank. Any authorized loan granted by a commercial bank to its parent holding company will be deducted from the bank’s core capital, directly impacting its regulatory Capital Adequacy Ratio. Furthermore, cross-board memberships are capped at 20 percent, while holding companies must maintain a regulatory capital buffer exceeding the combined minimum capital of their subsidiaries by at least 20 percent. The policy forbids banks from purchasing low-quality assets from struggling sister companies. It also bans the unconsented sharing of customer data and the utilization of depositor funds for affiliate operations. This structural ring-fencing follows the conclusion of Nigeria’s 24-month banking recapitalization exercise. The CBN is shifting focus toward risk containment as financial institutions aggressively expand into fintech and regional markets. Stakeholders and financial institutions have until July 9, 2026, to submit feedback on the draft framework before full implementation and enforcement under the Banks and Other Financial Institutions Act.

Nigeria’s Oil Output Hits 15-Month High, Exceeds OPEC Quota

LAGOS — Nigeria’s average daily crude oil production increased to 1.530 million barrels per day (bpd) in May 2026, marking a 15-month high and reinforcing its position as Africa’s top producer. Data from the Nigerian Upstream Petroleum Regulatory Commission (NUPRC) confirms output grew 2.77% month-on-month from April’s 1.489 million bpd. The growth reflects improved operational stability and zero major pipeline disruptions. The surge pushed Nigeria to 102% compliance with its 1.5 million bpd OPEC quota. This is the first time the country has outperformed its allocated target since mid-2025. Including an average daily condensate output of 170,446 barrels, Nigeria’s total hydrocarbon production for May reached 1.70 million bpd. This continues a steady five-month upward trajectory across upstream assets. The recovery was driven primarily by strong terminal performance. The Bonny Terminal led national output at 293,870 bpd, while the Forcados and Qua Iboe streams contributed 289,900 bpd and 173,360 bpd respectively. “In strict crude oil terms (excluding condensates), the 1.53 million barrels recorded in May 2026 represents the highest Nigeria has witnessed since January 2025 when crude oil production hit 1.538mbpd.” NUPRC said in a statement on X. “The latest crude oil production statistics thus represents a 15-month high On a month on month basis, production rose by 2.77% in May 2026 as against 1.48mbpd in April.” The NUPRC attributed the milestone to the successful completion of scheduled turnaround maintenance. Sustained asset protection also helped curb the historical infrastructure vulnerabilities that previously limited production capacity. The growth provides critical relief for Nigeria’s macroeconomic indicators. Rising output directly strengthens federal oil revenues and boosts foreign exchange liquidity amid the Central Bank’s ongoing economic stabilization reforms.

First Batch of 262 Nigerians Evacuated from South Africa Arrives in Lagos

LAGOS – A total of 262 passengers and three officials arrived at the Murtala Muhammed International Airport in Lagos on Thursday, marking the first batch of Nigerians evacuated from South Africa due to violent anti-immigration protests. The Ministry of Foreign Affairs confirmed that the repatriated citizens landed aboard an Air Peace flight. The operation was launched to protect nationals facing immediate security threats from escalating xenophobic hostilities. Foreign Affairs Minister Bianca Odumegwu-Ojukwu stated that “President Bola Tinubu ordered the emergency evacuation.” The directive targeted imperiled citizens who consider their lives at risk by their continued stay in South Africa. The evacuation follows a series of intense anti-migrant demonstrations shaking South Africa since April. Local mobs have demanded the removal of foreign workers, accusing them of taking jobs amidst a 30 percent unemployment rate. Tensions escalated sharply after South African citizen groups issued a strict June 30 ultimatum for undocumented migrants to leave. This timeline triggered widespread anxiety across diaspora communities, prompting immediate emergency interventions. The federal government approved five evacuation flights to accommodate the crisis. To ensure maximum safety for affected residents, the Nigerian High Commission in Pretoria extended its voluntary repatriation screening exercise until June 14. Over 1,000 Nigerians have registered for the voluntary repatriation exercise so far. Inter-agency teams received the first batch of 262 returnees in Lagos to provide immediate profiling, trauma counseling, and reintegration support. Nigeria joins other African nations, including Ghana, Malawi, and Mozambique, currently evacuating citizens from South Africa. Diplomatic engagement continues between Abuja and Pretoria to secure the safety of nationals remaining in the country.

Nigeria: Cardoso Snags Global ‘Central Bank of the Year’ Award in London as Reforms Pay Off

LAGOS — Central Bank of Nigeria (CBN) Governor Olayemi Cardoso formally received the prestigious 2026 Central Banking Central Bank of the Year Award here on Wednesday, signaling strong international approval of Nigeria’s aggressive monetary reforms. The award committee recognized the CBN’s swift return to orthodox monetary policy, decisive inflation-targeting measures, and foreign exchange market liberalization since Cardoso assumed office in late 2023. Accepting the honour, Cardoso framed the award as validation for institutional resilience, calling it an encouragement to sustain painful but necessary macroeconomic adjustments rather than a final destination for the apex bank. “According to the Governor, the Bank’s reform agenda has been guided by a clear objective: restoring confidence, strengthening institutional resilience and policy credibility, and laying a solid foundation for sustainable economic growth.” CBN stated in a post on X. The global recognition comes as Nigeria’s external reserves recently hit a ten-year high of $50 billion, providing a critical buffer for the volatile local currency amid ongoing monetary tightening. Foreign investors have lauded the bank’s structural transparency tools, including the Electronic Foreign Exchange Matching System, which effectively compressed the parallel market premium from over 60% to under 2%. Furthermore, investor sentiment improved dramatically after the CBN successfully cleared years of trapped foreign exchange forward obligations and secured Nigeria’s strategic exit from the Financial Action Task Force grey list. Crucially, the award closely follows the smooth conclusion of the CBN’s rigorous 24-month banking sector recapitalization program in March, which successfully shored up the capital bases of 33 commercial banks. Analysts note that this international endorsement gives the regulatory bank significant leverage as it continues to raise interest rates to curb sticky core inflation and stabilize domestic commodity prices. The London ceremony was attended by global financial policymakers, institutional investors, and central bank governors, highlighting Nigeria’s re-integration into the mainstream global financial ecosystem after years of unconventional interventions.

IMF backs Nigeria’s central bank on tight policy to beat inflation

LAGOS – The International Monetary Fund (IMF) has backed the Central Bank of Nigeria’s (CBN) tight monetary policy, urging a data-dependent approach until inflation is firmly defeated and public expectations anchor. In its 2026 Article IV Consultation report released on Tuesday, the IMF Executive Board endorsed a “tighter-for-longer” stance, validating the apex bank’s strategy to tackle resurgent consumer price pressures which hit a high of 15.69% in April. Directors welcomed the CBN’s progress toward adopting a full inflation-targeting framework, noting that clear communication and independent policy guidance will be vital to securing long-term price stability and market credibility. “The Central Bank of Nigeria should maintain a tight monetary policy stance with a data-dependent approach until disinflation is entrenched and inflation expectations are anchored.” IMF Directors said. “Directors welcomed progress toward adopting inflation targeting and encouraged steps to strengthen monetary transmission and communication.” IMF noted. The Washington-based lender also urged the central bank to implement institutional steps that strengthen monetary policy transmission, ensuring benchmark interest rate changes effectively influence commercial lending and deposit rates. Praising the commitment to a flexible exchange rate regime, the IMF noted the policy helped the naira appreciate 10% year-on-year against the U.S. dollar, while rebuilding external reserves to $46 billion in 2025. The Fund recommended that future foreign exchange interventions remain strictly limited to smoothing disorderly market volatility, while advising Nigeria to reduce dependency on volatile, short-term portfolio inflows. The IMF Executive Board welcomed recent tax reforms but noted that additional tax policy measures will likely be needed over the medium term to expand revenue collections. Furthermore, directors highlighted deep concerns regarding unrecorded off-budget expenditures and complex financing instruments, demanding immediate acceleration of public financial management reforms to strengthen fiscal reporting, transparency, and country risk frameworks. The Fund urged the government to urgently secure funding to scale up its structured cash transfer program, warning that acute poverty and food insecurity are expected to worsen under current global price pressures.

Nigeria’s Trade Surplus Soars 341% to ₦7.55 Trillion as Fuel Imports Plunge

LAGOS – Nigeria’s merchandise trade balance swung into a massive ₦7.55 trillion ($5.50 billion) surplus in the first quarter of 2026, driven by a sharp decline in refined petroleum imports and resilient crude oil export revenues. The National Bureau of Statistics (NBS) reported on Monday a stellar 341% quarter-on-quarter increase in trade surplus, providing critical macroeconomic relief for the country’s business landscape as structural fiscal pressures begin to ease. Total export values expanded by 11.63% from the preceding quarter to ₦21.17 trillion, representing 60.85% of entire trade, with crude oil sales accounting for 52.92% at ₦11.20 trillion. Concurrently, national import costs contracted sharply by 21.05% quarter-on-quarter to ₦13.62 trillion. This decline reflects a dramatic 81.38% drop in imported petroleum products, which plummeted to ₦748.10 billion. The contraction in fuel imports indicates shifting domestic energy supply logistics. This structural adjustment significantly lowered corporate demand for foreign exchange, helping stabilize local commercial banking transactions during the quarter under review. Corporate activities showed major structural changes. Industrial machinery and transport equipment dominated merchandise imports at ₦5.01 trillion, followed closely by manufactured goods, which totaled ₦8.48 trillion despite global logistical headwind pressures. Agriculture trade contracted as imports dropped 42.39% to ₦827.72 billion. Russia remained a key vendor, supplying ₦135.37 billion in durum wheat to help local mills mitigate ongoing food inflation concerns. On the export side, India maintained its position as Nigeria’s top commercial destination, purchasing ₦2.77 trillion of goods, while China led import suppliers with a dominant 37.42% market share. Logistical data showed that maritime transport handled 99.07% of outbound shipments. Apapa Port processed 73.14% of exports, while the newly commissioned Lekki Deep Sea Port secured a 15.53% share. This strong trade liquidity aligns with broader domestic reforms. In March 2026, the Central Bank of Nigeria successfully concluded its 24-month banking recapitalization program, structurally boosting institutional credit capacity across these trade sectors.

Nigeria Targets 95% Financial Inclusion by 2028 in Africa’s Largest Cashless Push

The Central Bank of Nigeria (CBN) targets 95% financial inclusion in Vision 2028, aiming to bring millions of unbanked citizens into the formal economy through aggressive infrastructure and digital identity reforms over the next 36 months. This target represents a significant leap from current tracking metrics. According to Enhancing Financial Innovation & Access (EFInA) latest financial access findings, Nigeria’s formal financial inclusion rate stands at 64%, leaving a multi-million citizen gap. The continental benchmark places Nigeria behind several regional peers. World Bank Findex metrics indicate that East and Southern African leaders like Kenya and South Africa boast formal inclusion rates exceeding 80% and 90% respectively, powered by mature mobile money ecosystems. The policy shift addresses persistent bottlenecks. Despite domestic electronic transactions exceeding 600 trillion naira in recent years, formal financial access remains starkly concentrated across urban centers, deeply marginalizing rural populations. To bridge this gap, the apex bank’s newly released Payment System Vision 2028 blueprint mandates that licensed financial operators achieve a 95% transaction success rate while strictly maintaining system uptimes of 99.999%. The strategy forces a pivot toward alternative transaction technologies. The central bank is mandating the deployment of offline-capable payment rails, utilizing Bluetooth and Near Field Communication to bypass rural network deficits. Gender disparities are also targeted. The CBN is rolling out a “Women Agent 2.0” pilot program to build trust and achieve gender parity across its nationwide network of two million banking agents. To protect grassroots consumers, the roadmap enforces automated identity verification. Moving forward, the apex bank requires systematic, real-time harmonization of Bank Verification Numbers (BVN) and National Identification Numbers (NIN) across all wallets. Furthermore, the framework introduces a centralized National Consumer Redress Portal. This ombudsman structure binds financial institutions to automated service level agreements, targeting a mandatory 90% dispute resolution rate to restore public trust. The aggressive rollout follows recent regulatory challenges. Over the past year, the CBN faced severe public scrutiny regarding cash availability, network downtime during currency transitions, and rising multi-channel fintech fraud. In response, the document outlines an auxiliary goal targeting a 70% reduction in financial fraud losses, supported by a newly established 24/7 National Payment Security Operations Centre for automated threat monitoring. Execution occurs across three distinct phases. The apex bank will initiate joint technical working groups immediately, moving into predictive artificial intelligence fraud analytics and full cross-border payment integration by 2028.

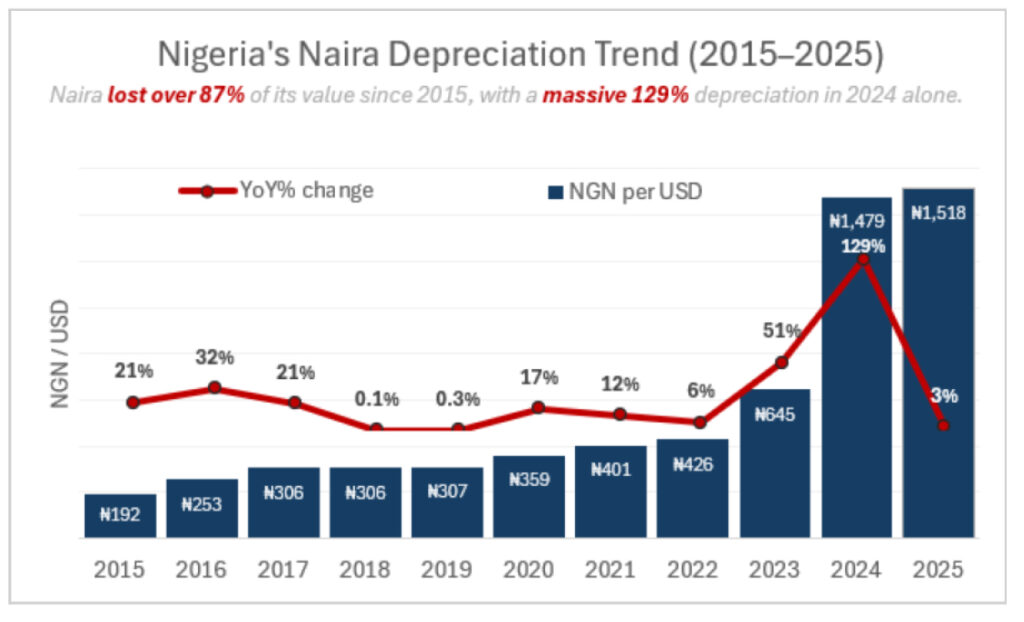

Exclusive: Nigeria’s SEC to provide update on capital recapitalization end June

LAGOS – The Securities and Exchange Commission (SEC) is set to evaluate compliance plans submitted by operators and provide key updates by the end of June 2026, following sweeping hikes to minimum capital requirements; source familiar with the matter told ThinkBusiness Africa. The capital market regulator issued the directive in January 2026, mandating capital threshold increases of up to 3,400%. Brokerage operators must achieve full financial compliance with the new benchmarks on or before June 30, 2027. This mid-year review follows an initial April 2026 deadline for market intermediaries to submit board-approved recapitalization strategies. Intermediaries failing to meet structural conditions face potential license downgrades or forced corporate mergers. The policy aims to fix a decade of regulatory stagnation under the previous 2015 framework. That older system left firms exposed to severe naira depreciation and rising market complexities. Official financial data indicates the Nigerian naira lost more than 87% of its value between 2015 and 2025. A severe 129% currency drop in 2024 alone eroded real capital buffers. A weekly institutional brief from Africa Business convention (ABC) highlights severe structural gaps facing independent operators under these rules. For instance, standard broker-dealers face an aggressive 567% statutory increase from N300 million to N2 billion. Full-scope tier-1 fund managers face a massive hike from N150 million to N5 billion. It also noted that the earlier January circular was a correction of accumulated distortion, not a routine review and investors should see it as a signal that Nigeria’s regulatory posture has “shifted from maintenance to transformation”. However, the SEC’s recapitalization structure mirrors a parallel multi-trillion naira consolidation exercise executed across Nigeria’s banking sector. Between 2024 and 2026, domestic commercial banks raised N4.65 trillion in fresh equity capital. Regulatory authorities are utilizing fixed statutory floors to eliminate high industry fragmentation. The market currently hosts roughly 200 dealing firms, many possessing highly limited risk-absorption capacities. The upcoming June update will categorize compliant firms, pending structural mergers, and operators adjusting license scopes. This shift repositions local institutions to attract cross-border capital flows under regional trade frameworks.

Nigeria’s Capital Market Recapitalisation Revisited

Nigeria’s capital market is entering one of its most significant restructuring phases in more than a decade. In January 2026, the Securities and Exchange Commission (SEC) introduced revised minimum capital requirements for capital market operators, increasing the financial thresholds by as much as 3,400% required for firms to operate across multiple market segments and setting a June 30, 2027 deadline for full compliance. The reform comes after more than ten years of regulatory stagnation. The previous capital framework was introduced in 2015, when the naira traded at approximately ₦200 to the US dollar and Nigeria’s financial ecosystem was considerably less complex. Since then, inflation, currency depreciation, technological innovation, and the emergence of new asset classes have fundamentally altered the operating environment. Yet the minimum capital requirements governing market operators remained largely unchanged. Source: Nigeria’s official exchange rate (Nigerian naira per US$) 2015 – 2025 Over time, this created three major challenges. First, the sharp depreciation of the naira significantly reduced the real value of existing capital thresholds, weakening their effectiveness as measures of financial strength and risk absorption capacity. Second, the framework no longer reflected the realities of a modern capital market, failing to adequately account for digital asset operators, fintech-driven investment platforms, commodity market intermediaries, and other emerging segments. Third, the industry became increasingly fragmented, with many operators possessing limited balance sheet capacity despite growing transaction volumes and market complexity. The SEC’s recapitalisation initiative seeks to address these structural weaknesses by strengthening the financial resilience of market operators, improving investor protection, supporting larger and more sophisticated market activities, and enhancing the competitiveness of Nigeria’s capital market. The reform also aligns with broader efforts to modernise the country’s financial sector and deepen domestic capital formation at a time when Nigeria is seeking to attract greater levels of local and international investment. The initiative follows a wider trend of recapitalisation across Nigeria’s financial system. Between 2024 and 2026, the banking sector recapitalisation programme mobilised approximately ₦4.65 trillion in fresh equity capital and contributed to stronger market confidence, with the NGX All-Share Index reaching record highs during the period. The SEC’s reform represents a similar attempt to build stronger institutions capable of supporting long-term economic growth. Source: NGX, 2026 This brief sets out to examine the rationale behind the SEC’s capital threshold raise, the shortcomings of the previous framework, the key changes introduced under the new regime, and the implications for market operators, investors, and the future structure of Nigeria’s capital market. Key Takeaway: The 2015 capital framework was rendered structurally inadequate by naira depreciation, market complexity, and a fragmentation of the intermediary base that left Nigeria’s capital market unable to execute transactions at a size commensurate with the country’s economic ambitions. The January 2026 circular is a correction of accumulated distortion, not a routine review. Investors should read it as a signal that Nigeria’s regulatory posture has shifted from maintenance to transformation. RECAPITALIZATION: A BROADER FINANCIAL SECTOR PATTERN Nigeria’s capital market recapitalisation does not stand in isolation. It is part of a broader pattern of financial capacity strengthening across the financial system, where regulators repeatedly use capital thresholds as a structural tool to reshape institutions, improve resilience, and expand scale. A key precedent is the 2004–2005 banking consolidation, which reduced the number of banks from over 80 to 25 after a sharp increase in minimum capital requirements. That reform fundamentally strengthened the banking system, created larger balance sheets, and enabled regional expansion across West Africa. More recently, the 2024–2026 banking recapitalisation cycle required banks to raise substantial new equity in response to macroeconomic pressures and currency volatility. The exercise produced no institutional failures, strengthened systemic stability, and contributed to a record rally in the NGX All-Share Index, which reached 201,287 points, while also bringing in an estimated half a million new retail investors through equity issuance activity. Against this backdrop, Nigeria is currently running three concurrent recapitalisation exercises across banking, insurance, and capital markets within a 36-month window, all aligned directly or indirectly with the broader ambition of building a $1 trillion economy. The banking exercise has already been completed, the insurance reform is ongoing, and the SEC capital market reform runs from 2026 to 2027. For investors, this is not a series of isolated reforms but a coordinated expansion of capital requirements across the entire financial intermediary system. Key Takeaway: Nigeria’s banking, insurance, and capital market recapitalisations represent a single coordinated restructuring of the financial system within one policy cycle. For investors, the key constraint is not regulatory ambition but capital absorption capacity, as successive sectors compete for the same pool of equity funding within a compressed timeframe. AFRICAN PRECEDENTS: HAS ANY MARKET DONE THIS BEFORE? Nigeria is not the first African market to raise capital requirements for market operators. Kenya’s 2025 capital markets reforms introduced a tiered broker-dealer structure, increased capital thresholds across key operator categories, and extended requirements to trustees and custodians. Like Nigeria’s current exercise, the reforms were designed to strengthen institutional capacity and support market consolidation. The Kenyan experience shows how higher capital standards can be used to reshape industry structure rather than simply improve compliance. South Africa offers a more advanced benchmark. The Financial Sector Conduct Authority operates a risk-based capital framework where requirements are linked to income, assets under management, and risk exposure rather than fixed minimums alone. The system also covers a broader range of market participants, including hedge funds and derivatives intermediaries. This demonstrates the direction many mature markets have taken as they move beyond static capital thresholds toward continuous prudential supervision Egypt provides a cautionary example. Although capital adequacy reforms were introduced in 2021, repeated deadline extensions weakened enforcement and limited the intended consolidation of the sector. For Nigeria, this highlights that regulatory credibility is as important as policy design, particularly as operators approach the June 2027 compliance deadline. THE NEW ARCHITECTURE: WHAT CHANGED, BY HOW MUCH, AND FOR WHOM Tiered, Risk-Differentiated Thresholds Across Operator Categories The most important change in the new Securities and Exchange Commission (SEC) capital framework is not only the increase in minimum capital levels, but

Nigeria Private Sector Activity Hits 9-Month High Amid Stiff Cost Pressures

LAGOS – Nigeria’s private sector logged its strongest expansion in nine months as the S&P Global Purchasing Managers’ Index jumped 3.24% to 54.1% in May from 52.4 in April. The headline reading signaled a solid monthly improvement in business conditions across the country. The health of the private sector has now strengthened for four consecutive months. Accelerated expansions in both output and new orders drove the growth. Anecdotal evidence from surveyed firms pointed to improving customer demand and the successful launch of new products. Output growth was recorded across manufacturing, agriculture, services, and wholesale and retail sectors. Improving demand led companies to aggressively expand their purchasing activity and inventories during the month. Efforts to secure inputs were helped by an improvement in vendor performance. Prompt payments and better road conditions helped to speed up supplier delivery times. Despite rapid growth, employment rose only slightly midway through the second quarter. Sustained job creation has now been recorded on a monthly basis for an entire year. Meanwhile, backlogs of work increased for the fourth successive month. Firms blamed customer payment delays, raw material shortages, and recurrent power failures for the persistent operational delays. Increasing fuel costs following geopolitical tensions in the Middle East drove up purchase prices. Purchase costs rose rapidly again, despite the overall rate of cost inflation easing. Output prices continued to rise sharply as firms passed expenses to consumers. Manufacturing and agriculture experienced the steepest increase in output prices as firms defended margins. This private sector rebound follows a weaker-than-expected first-quarter real GDP growth rate of 3.89%, which was dragged down by a slowing non-oil sector. The policy environment remains highly restrictive for businesses. The Central Bank of Nigeria recently held its benchmark interest rate at 26.5% to curb stubborn inflationary pressures. National Bureau of Statistics data showed headline inflation quickened to 15.69 percent in April. Elevated transport and food prices continue to pinch corporate margins and consumer wallet share.